The HSA Proportional Contribution Limit

By Brian Gilmore | Published July 17, 2020

Question: What is the HSA contribution limit for an employee who is enrolled in an HDHP for only a portion of the year?

Short Answer: The standard rule is that the employee will have a proportional contribution limit based on the months of HSA eligibility, but in certain circumstances, the last-month rule will allow the employee to contribute to the full statutory limit.

General Rule: HSA Eligibility

The general rule is that an individual must meet two requirements to be HSA-eligible (i.e., to be eligible to make or receive HSA contributions):

Be covered by an HDHP; and

Have no disqualifying coverage (generally any medical coverage that pays pre-deductible, including Medicare).

HSA eligibility also requires that the individual cannot be claimed as a tax dependent by someone else.

For more details on everything HSA, see our Newfront Go All the Way With HSA Guide.

HSA Contribution Limits: Calendar Year Limit

HSA contribution limits are based on the calendar year. They are not related to the employer’s HDHP plan year.

The HSA contribution limits are adjusted annually for inflation, currently at the following levels:

2020 Contribution Limits

Individual HDHP Coverage: $3,550

Family HDHP Coverage: $7,100

2021 Contribution Limits

Individual HDHP Coverage: $3,600

Family HDHP Coverage $7,200

Family HDHP coverage includes the employee plus at least one other individual (spouse, domestic partner, child(ren)) covered.

A $1,000 catch-up contribution is available for individuals who are at least age 55 by the end of the calendar year. The $1,000 annual catch-up contribution limit has been fixed since 2009 and will not adjust further for inflation. For more details, see our previous post: HSA Catch-Up Contributions.

For more details on the other HDHP/HSA annual limits, see our Compliance Alert: IRS Releases 2021 Inflation Adjusted Amounts for HSAs.

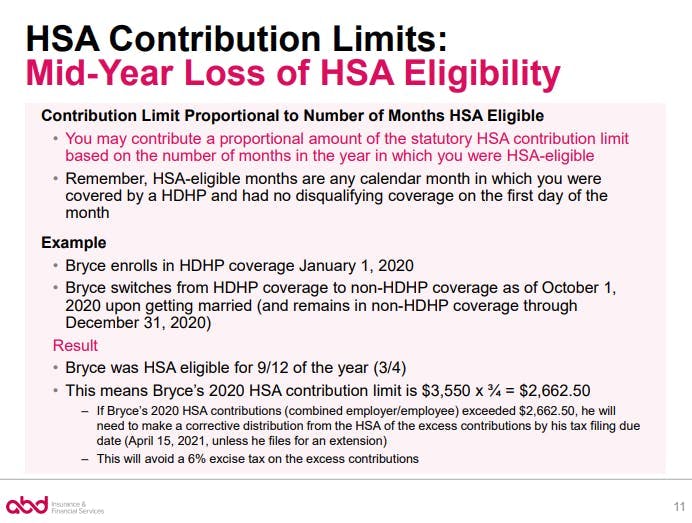

The Proportional Contribution Limit: Partial Year of HSA Eligibility

The standard rule is that employees who are HSA-eligible for only a portion of the calendar year have a reduced HSA contribution limit. The reduced contribution limit is a proportional amount based on the number of months of HSA eligibility for the employee in the calendar year. HSA eligibility is determined as of the first day of each calendar month.

Example 1:

Bryce enrolls in employee-only HDHP coverage with his employer on January 1, 2020 (and has no disqualifying coverage).

Bryce changes to standard HMO coverage as of October 1, 2020 upon getting married, and he remains in that non-HDHP coverage through the end of 2020.

Result 1:

Bryce is HSA-eligible for nine months of the calendar year.

Bryce’s HSA contribution limit is therefore 9/12 (3/4) of the statutory limit.

This means Bryce’s HSA proportional contribution limit is $3,550 x ¾ = $2,662.50

The IRS provides a useful chart and worksheet for determining your HSA contribution limit in the “Line 3 Limitation Chart and Worksheet” section of the Form 8889 Instructions. This worksheet also incorporates the proportional catch-up contribution amount, as well as how changes from individual to family coverage affect the contribution limit.

Individuals who contribute in excess of the proportional limit will need to take a corrective distribution of the excess contributions by their tax filing deadline (generally April 15 without extension) to avoid a 6% excise tax on the excess contributions. For more details, see our previous post Excess HSA Contributions, as well as slide 53 of our Newfront Go All the Way With HSA Guide.

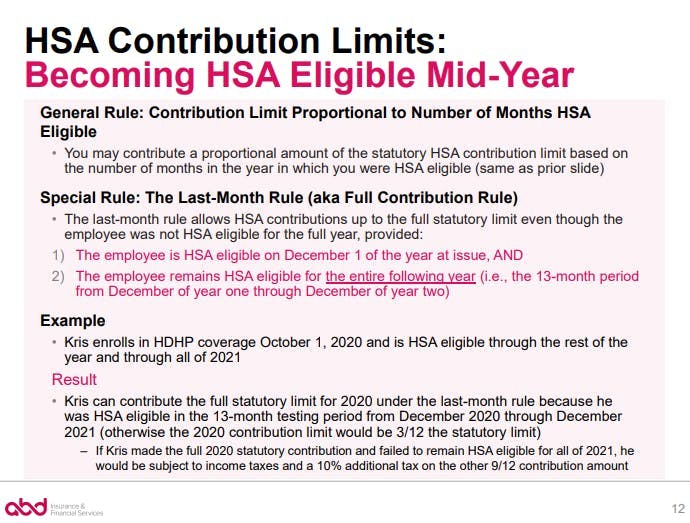

The Last-Month Rule: An Exception that Permits the Full Contribution Limit

Employees who enroll in the HDHP mid-year are generally subject to the proportional contribution limit above. However, a special rule known as the “last-month rule” may apply to permit the mid-year enrollee to contribute up to the full statutory limit—even though the employee was not HSA-eligible for the full calendar year.

In order to qualify for the last-month rule, the employee must satisfy both of the following two conditions:

The employee is HSA-eligible on December 1 of the year at issue; AND

The employee remains HSA-eligible for the entire following calendar year.

This creates a 13-month “testing period” that applies to determine whether the individual has met the last-month rule requirements. The mid-year HDHP enrollee must be eligible on December 1 through the entire subsequent calendar year to contribute up to the full statutory limit (as opposed to the standard proportional limit) for the year in which the employee enrolled in the HDHP mid-year.

Example 2:

Kris enrolls in HDHP coverage on October 1, 2020 and is HSA-eligible continuously through the end of 2021.

Result 2:

Kris can contribute up the full statutory limit (as opposed to the standard proportional limit) in 2020 by taking advantage of the last-month rule.

Kris qualifies for the last-month rule in 2020 because he was HSA-eligible in the 13-month testing period from December 1, 2020 through December 2021.

If Kris had not qualified for the last-month rule, his contribution limit would have been 3/12 (1/4) of the contribution limit.

The IRS also provides a useful summary of the last-month rule in Publication 969 and the Form 8889 Instructions.

Mid-year HDHP enrollees who contribute to the statutory limit but do not satisfy the 13-month testing period by failing to remain HSA-eligible will be subject to income taxes and a 10% additional tax on the amounts contributed in excess of the statutory limit. For more details, see slide 54 of our Newfront Go All the Way With HSA Guide.

Non-Calendar HDHP Plan Years: How the Contribution Limit Applies

The HSA contribution limit is based on the calendar year—it is not based on the plan year of the employer’s HDHP.

Where the employer has a non-calendar plan year, the employee will make an HSA contribution election based on that non-calendar plan year. Those contributions will be spread out over the full plan year and contributed ratably over each payroll period. Therefore, a prorated portion of the HSA election will be contributed in calendar year one, and a prorated portion of the HSA election will be contributed in calendar year two.

The end result is that an employee’s HSA election will not create issues with the proportional HSA contribution limit because the prorated portion of the election contributed in each calendar year will not exceed the employee’s standard proportional limit.

Example 3:

Kristen’s employer sponsors an HDHP with a 10/1 plan year.

Kristen elects to enroll in employee-only coverage under HDHP for the first time at open enrollment for the plan year beginning 10/1/20.

Kristen’s employer contributes $1,000 to employees enrolled in employee-only HDHP coverage with per payroll contributions.

Kristen elects to contribute $2,550 based on the maximum employee-only contribution limit after taking into account the employer contribution.

Result 3:

Kristen will make and receive HSA contributions of $887.50 in calendar year 2020 based on the employer contribution ($250) and her contributions ($637.50) in October through December.

Kristen will make and receive HSA contributions of $2,662.50 in calendar year 2021 based on the employer contribution ($750) and her contributions ($1,912.50) in January through September.

Her contributions will therefore not exceed the standard proportional contribution limit for either calendar year.

Additional Example 3 Notes:

If Kristen wanted to utilize the last-month rule in 2020 to contribute in excess of the $887.50 proportional limit, she would need to commit to electing the HDHP again at open enrollment for the 10/1/21 plan year to maintain HSA eligibility through December 2021.

Kristen would make any 2020 last-month rule contributions in excess of $887.50 outside of payroll by directly contributing to the HSA custodian and taking an above-the-line deduction. The Section 125 rules, which govern employee HSA pre-tax payroll contributions, would generally prohibit front-loading the HSA contributions through payroll. See our previous post for more details: Employee HSA Front-Loading.

Kristen could slightly increase her election in 2021 to take advantage of the slightly higher contribution limit ($50 increase to $3,600) by taking advantage of the ability to change HSA contribution elections for any reason at least once per month. See our previous post for more details: HSA Contribution Election Changes.

Regulations

IRC §223(b)(8):

(8) Increase in limit for individuals becoming eligible individuals after the beginning of the year.

(A) In general. For purposes of computing the limitation under paragraph (1) for any taxable year, an individual who is an eligible individual during the last month of such taxable year shall be treated—

(i) as having been an eligible individual during each of the months in such taxable year, and

(ii) as having been enrolled, during each of the months such individual is treated as an eligible individual solely by reason of clause (i), in the same high deductible health plan in which the individual was enrolled for the last month of such taxable year.

(B) Failure to maintain high deductible health plan coverage.

(i) In general. If, at any time during the testing period, the individual is not an eligible individual, then—

(I) gross income of the individual for the taxable year in which occurs the first month in the testing period for which such individual is not an eligible individual is increased by the aggregate amount of all contributions to the health savings account of the individual which could not have been made but for subparagraph (A), and

(II) the tax imposed by this chapter for any taxable year on the individual shall be increased by 10 percent of the amount of such increase.

(ii) Exception for disability or death. Subclauses (I) and (II) of clause (i) shall not apply if the individual ceased to be an eligible individual by reason of the death of the individual or the individual becoming disabled (within the meaning of section 72(m)(7)).

(iii) Testing period. The term “testing period” means the period beginning with the last month of the taxable year referred to in subparagraph (A) and ending on the last day of the 12th month following such month.

IRS Publication 969:

https://www.irs.gov/pub/irs-pdf/p969.pdf

Last-month rule.

Under the last-month rule, if you are an eligible individual on the first day of the last month of your tax year (December 1 for most taxpayers), you are considered an eligible individual for the entire year. You are treated as having the same HDHP coverage for the entire year as you had on the first day of the last month if you didn’t otherwise have coverage.

Testing period.

If contributions were made to your HSA based on you being an eligible individual for the entire year under the last-month rule, you must remain an eligible individual during the testing period. For the last-month rule, the testing period begins with the last month of your tax year and ends on the last day of the 12th month following that month (for example, December 1, 2019, through December 31, 2020).

If you fail to remain an eligible individual during the testing period, for reasons other than death or becoming disabled, you will have to include in income the total contributions made to your HSA that wouldn’t have been made except for the last-month rule. You include this amount in your income in the year in which you fail to be an eligible individual. This amount is also subject to a 10% additional tax. The income and additional tax are calculated on Form 8889, Part III.

Newfront Go All the Way With HSA Guide

Mid-Year Loss of HSA Eligibility

Becoming HSA Eligible Mid-Year

Brian Gilmore

Lead Benefits Counsel, VP, Newfront

Brian Gilmore is the Lead Benefits Counsel at Newfront. He assists clients on a wide variety of employee benefits compliance issues. The primary areas of his practice include ERISA, ACA, COBRA, HIPAA, Section 125 Cafeteria Plans, and 401(k) plans. Brian also presents regularly at trade events and in webinars on current hot topics in employee benefits law.

Connect on LinkedIn