What is CalSavers? What Employers Should Know About the Program and Its Alternatives

Published December 2, 2020

In 2016, California passed legislation that created the CalSavers Retirement Savings Program. The program was designed to give the nearly 7.5 million private-sector employees without access to a retirement plan a chance to save for their future.

What is CalSavers?

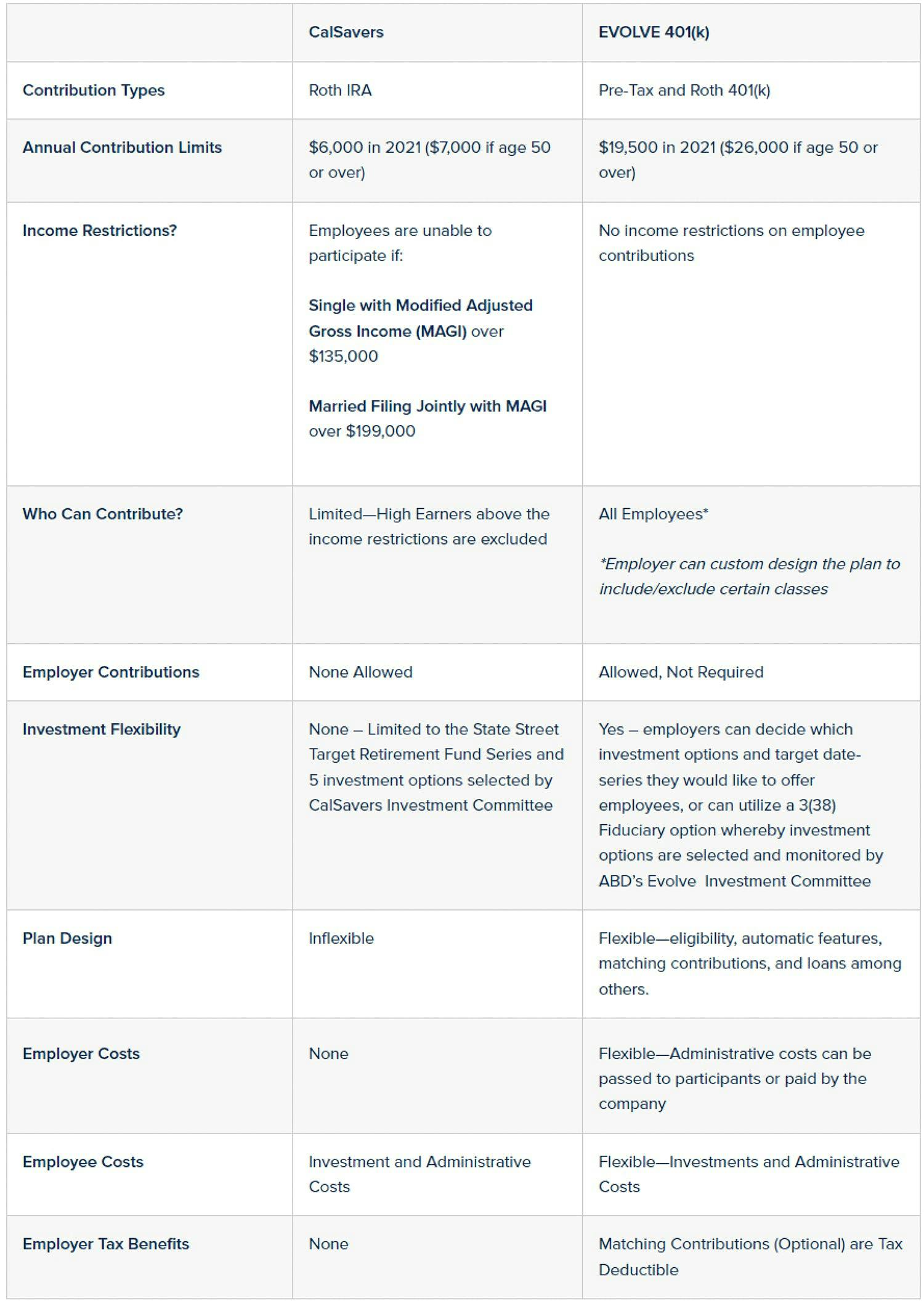

“CalSavers” created a state sponsored retirement program with a structure very similar to a Roth Individual Retirement Account (IRA), for employees whose employers do not offer them a retirement plan at work.

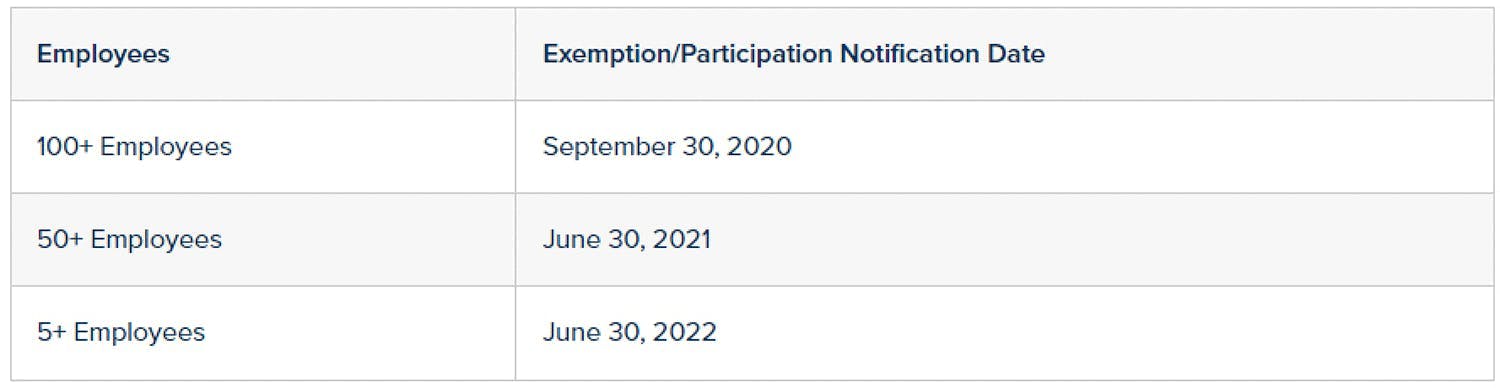

Beginning in 2020 and running through 2022, small businesses with more than 5 employees are required to offer a retirement savings option to their employees. Employers can either sponsor their own plan, e.g. a 401(k) plan, or register for CalSavers. It is important to take action as noncompliance can result in fines ranging from $250 to $500 per employee.

What if you already offer your employees an employer sponsored plan? That’s great! You will need to notify the state by certifying your plan exemption online here.

You’ll need three pieces of information to certify your exemption or register for CalSavers:

Federal Employer Identification or Tax Identification Number (EIN/TIN)

CA Employer Payroll Tax Account Number (from EDD)

CalSavers access code from your notification (CalSavers notifies affected plans either via email or a letter in the mail. If you have difficulty locating this code, you can request online here or call 855-650-6916)

Employers will need to indicate exemption or sign-up to participate in CalSavers by the following dates:

Unlike a 401(k) plan, CalSavers is established, operated, and maintained by the state of California.

Employers do not have discretion to determine the terms of the IRAs, the investments offered, or the plan design, e.g. no employer contribution. Employer responsibilities are limited to registering for the program, providing roster information for their employees, and deducting contributions from employee paychecks/submitting them to CalSavers.

Employees, on the other hand, are responsible for opting in or out of the program and selecting their investments. If they do nothing, employees are automatically enrolled in the program at 5% of their gross income by their employer. There is also an automatic increase feature that increases employee’s savings rate by 1% annually until employee’s savings rate reaches 8%, unless employees choose otherwise. Their contributions will be defaulted into the money market fund until their balance reaches $1,000, upon which their money is transferred into an age appropriate Target Date Fund based on their date of birth.

Why might an employer opt to start their own 401(k) plan versus opting in to CalSavers? For one, high earners—those making over $135,000 if single, or $199,000 if married filing joint— are ineligible to participate in CalSavers due to their high earners status, and will have to manually opt-out of the program or notify their employer of their high earner status ineligibility. If your company employs high earners or is considering employing high earners, a 401(k) plan may be a better fit since as they are not subject to any income restrictions.

Second, a traditional 401(k) plan offers far greater savings potential! Participants can save up to $19,500 through a 401(k) plan in 2021 ($26,000 if over age 50), while CalSavers caps contributions at $6,000. Participants can save up to an additional $13,500 in a 401(k) plan versus CalSavers!

A 401(k) plan offers additional flexibility and choice, both for employers and employees. CalSavers may be a good option for companies that are comfortable with the limited flexibility, have a fixed employee headcount, or do not anticipate staffing high earners. A 401(k) plan, however, may be a better fit for employers that are looking for investment flexibility, vendor flexibility with expanded tools & resources, anticipate a growing headcount, or foresee employing high earners in the future.

If you are considering offering a 401(k) plan, we would love to chat with you. We understand that offering a 401(k) plan can be new territory—and when you’re managing a business, you need to manage your resources wisely. EVOLVE 401(k) offers full-service retirement benefits while keeping costs in check. With EVOLVE, you can offer a nationally recognized 401(k) plan that helps you compete with larger employers, without the extra hassle or cost. We help you and your team procure a cost-effective plan that meets your business needs and scales with your growth.

To learn more about EVOLVE 401(k), we encourage you to take a look at our Retirement Services website. For more information about CalSavers please visit the CalSavers website.

The table below provides an overview of CalSavers versus EVOLVE 401(k), which we hope helps you determine which plan is the right fit for your employees!