Significant HSA Contribution Limit Increase for 2023

By Brian Gilmore | Published May 4, 2022

Executive Summary

The IRS has issued its annual inflation adjustment to the HSA contribution limits for calendar year 2023. With inflation at unusually high levels, we will also have unusually high increases to the HSA contribution limits.

The 2023 HSA contribution limits are as follows:

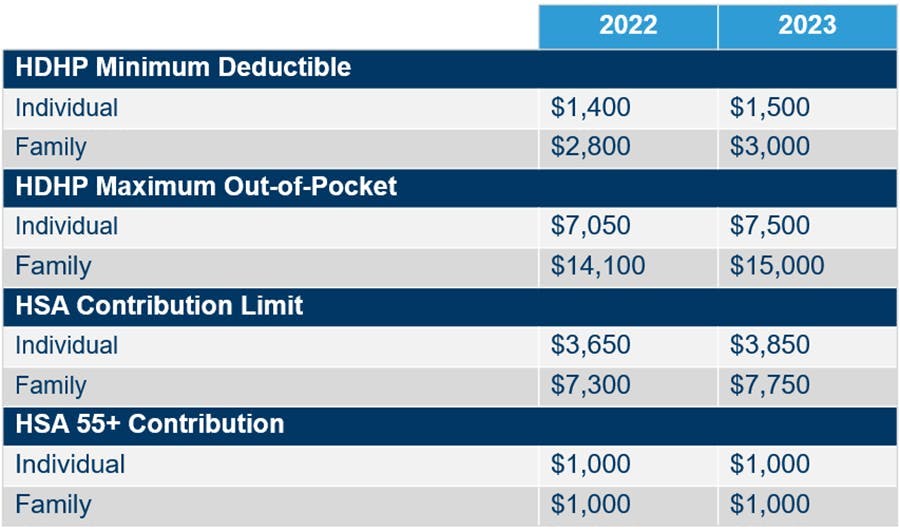

Individual Coverage: $3,850 ($200 increase)

Family Coverage: $7,750 ($450 increase)

2023 Inflation Adjusted Amounts for HSAs and HDHPs

The IRS has released its annual update announcing the HSA contribution limit increases for 2023. These cost-of-living adjustments are based on the Chained Consumer Price Index for All Urban Consumers (C-CPI-U).

The full guidance is available here:

With inflation running higher than normal (the most recent March 2022 12-month C-CPI-U inflation increase is at 8.1%), we were due for an unusually large HSA contribution increase to reflect the higher cost of living. We got that and more with a much larger than normal $200 and $450 increase to the individual and family coverage HSA contribution limits, respectively.

The 2023 calendar year HSA contribution limits are as follows:

The 2023 HSA contribution limit for individual coverage increases by $200 to $3,850.

The 2023 HSA contribution limit for family coverage (employee plus at least one other covered) increases by $450 to $7,750.

Note: The age 55+ catch-up contribution limit of $1,000 is fixed by law and does not adjust for inflation.

The annual update also includes the 2023 calendar year minimum deductible and out-of-pocket maximums allowed for a plan to qualify as a high deductible health plan (HDHP)—the required coverage for an individual to be eligible to make or receive HSA contributions.

The 2023 HDHP inflation adjusted amounts are as follows:

The 2023 minimum deductible for individual coverage increases by $100 to $1,500.

The 2023 minimum deductible for family coverage increases by $200 to $3,000.

The 2023 maximum out-of-pocket limit for individual coverage increases by $450 to $7,500.

The 2023 maximum out-of-pocket limit for family coverage will increase by $900 to $15,000.

Table of 2023 Inflation Adjusted HSA Amounts:

Additional HSA Updates: Preventive Care, CARES Act, CAA, CAA 2022, and More!

After remaining relatively stable for an extended period since the HSA inception point in 2004, HSAs have experienced a whirlwind of enhancements in recent years. Although none of the changes by themselves are revolutionary, the modifications are significant in the aggregate.

Taken together, these changes have significantly improved HDHPs and HSAs by increasing reimbursable expenses and eliminating unnecessary barriers to eligibility:

First-Dollar Telehealth Relief (effective April 2022 – December 2022)

CAA 2022 extends prior expiring CARES Act relief to provide that HDHPs may provide first-dollar telehealth and other remote care services for the months of April 2022 – December 2022.

No Surprises Act (effective for plan years beginning on or after January 1, 2022)

HSA eligibility and HDHP status is not affected by surprise billing benefits made under the CAA’s No Surprises Act provisions (or similar state law protections).

Full details: CAA Surprise Billing Rules Preserve HSA Eligibility

Personal Protective Equipment (effective for expenses incurred on or after January 1, 2020)

HSAs (and FSAs and HRAs) may reimburse PPE such as masks, hand sanitizer, and sanitizing wipes for the primary purpose of preventing the spread of Covid.

Menstrual Care Products (effective for expenses incurred on or after January 1, 2020)

HSAs (and FSAs and HRAs) may reimburse menstrual care products—including tampons, pads, liners, cups, sponges, or other similar products.

Full details: How the CARES Act Affects Employee Benefits

Over-the-Counter Medicines and Drugs (effective for expenses incurred on or after January 1, 2020)

HSAs (and FSAs and HRAs) may reimburse over-the-counter medicines and drugs without the need for a prescription.

Full details: How the CARES Act Affects Employee Benefits

Free Covid Testing (effective March 2020)

Plans will not fail to maintain HDHP status if they provide first-dollar coverage for medical care services and items purchased related to testing for and treatment of Covid.

Expansion of Preventive Care Services (effective July 2019)

Expansion of HDHP first-dollar coverage availability to include medical services and items to prevent exacerbation of a chronic condition.

Full details: IRS Expands Definition of Preventive Care for HDHPs

For more details on everything HDHP/HSA, see our 2022 Newfront Go All the Way With HSA Guide.

Brian Gilmore

Lead Benefits Counsel, VP, Newfront

Brian Gilmore is the Lead Benefits Counsel at Newfront. He assists clients on a wide variety of employee benefits compliance issues. The primary areas of his practice include ERISA, ACA, COBRA, HIPAA, Section 125 Cafeteria Plans, and 401(k) plans. Brian also presents regularly at trade events and in webinars on current hot topics in employee benefits law.

Connect on LinkedIn