Prep for a Recession: Get Back to Money Management Basics in Five Steps

By Michael Forney | Published February 2, 2023

In 2022, we experienced inflation numbers not seen since the early 1980s, geopolitical instability from Russia’s invasion of Ukraine, financial market declines, and the rapid rise of interest rates. All of that has led to increased pressure on wallets and predictions from economists and business leaders that a recession is on the horizon. However, there are some simple steps to take care of your personal finances, whatever the economic outcome.

**What is a recession?**While a recession is a general decline in economic activity, it can be more specifically defined as two negative quarters of GDP growth, which we experienced in 2022. Other factors taken into consideration include the labor market, industrial output, and consumer spending.

**What can we do about it?**The factors for a recession are largely outside of our individual control, but we can protect our personal finances by returning to the basics of money management. A recessionary period requires us to “tighten our belts” and hone in on spending habits.

**Step one: Examine your expenses.**Pull up your expenses from last year with these questions in mind:

On average, how much did you spend per month?

On average, how much money did you make per month?

How much did you spend on non-negotiables (rent, utilities, phone, etc.)?

How did you spend your discretionary cash flow (or “leftover” money)?

How much did you save?

Once you’ve identified how you spent your money, identify trouble areas. Ask yourself:

Where did you spend too much?

How can you reallocate dollars to be more reflective of your values or goals?

What are your needs and wants?

Are there any subscription services that you can afford to cancel?

**Step two: Create a budget.**With that evaluation in hand, you can begin building out a plan for 2023 and beyond. Put together a cash flow plan. To do this, list out the following items:

Expected monthly income

Expected federal, state, and local tax withholdings

Expected monthly expenses

Goals (e.g., retirement savings, major purchases, or vacations)

Once you build this budget, stick to it. Consider using an app or software — such as Mint, Personal Capital, or Quicken — to track expenses. Another option is a robo-advisor, which uses computer algorithms to advise you on how to allocate your investments. In some cases, robo-advisor platforms also provide access to a human financial advisor for basic questions. However, if you can afford to do so, it may be best to work with a certified financial planner (CFP), who can provide holistic advice on the entire breadth of your finances, ranging from cash flow and debt management to insights on retirement and estate planning.

Step three: Build an emergency fund.

It’s generally advisable to have 3 to 6 months of non-negotiable (or essential) living expenses in an emergency fund should you have unforeseen expenses or an emergency. If you have limited needs, you might gravitate toward the 3-month end of the spectrum. Conversely, if you have more financial responsibilities, you may gravitate towards the higher end of the spectrum. It depends on your situation and what is most comfortable for you. Additionally, if you are a business owner, you might hold 6 to 12 months of essential expenses because of your risk profile, particularly as a recession closes in.

To establish your fund, figure out what your discretionary cash flow is going to be (i.e., money left over after expenses). From there, determine what portion you would like to allocate to the emergency fund. This could be a couple dollars per month, hundreds, or even thousands. The more money you save, the more quickly you can build up the fund.

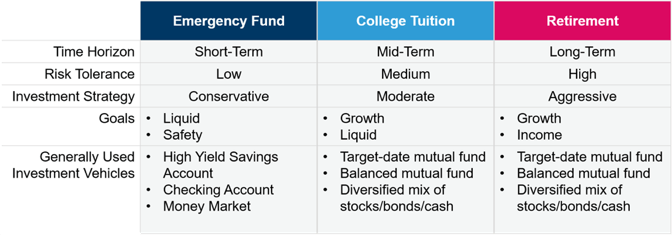

Step four: Outline a savings strategy.

How we save and what vehicle we utilize will be dictated by our specific goals, risk tolerance, and how soon we need to access those funds. Generally, the shorter the time horizon (e.g., 1 to 3 years), the less risk we can afford to take, and the longer the time horizon (e.g., 5+ years), the more risk we can afford to take. Here are some examples:

As the table illustrates, different goals utilize different investment vehicles. An emergency fund may use a basic checking or high yield savings account. On the other hand, retirement savings will likely utilize a retirement account like an IRA or 401(k).

**Step five: Take advantage of rewards and benefits.**Just as we may take advantage of cash back or rewards on our credit cards, employee benefits can help fill in the gaps during times of financial constraint. You might have an EAP which can help pay for things like counseling, or you may have a gym membership offering. EAPs might also include financial wellness benefits, such as a financial advisor or student loan assistance. Whatever the case, take advantage of any benefits which can help you save money in 2023.

Michael Forney

Investment Advisor and Financial Wellness Specialist

Michael is an Investment Advisor and Financial Wellness Specialist focusing on providing employee education and partnering with clients on financial wellness strategies. He possess a depth of knowledge on employer sponsored retirement plans, particularly the 401(k), and has a broad range of financial knowledge on investments, high-level tax benefits of various retirement accounts, and savings strategies. Previously, Michael worked at a top producing advisory firm where he built financial plans for families and businesses as a Financial Planning Specialist.

Connect with Michael on LinkedIn