HSAs for Veterans

By Brian Gilmore | Published August 31, 2018

Question: How does a veteran’s eligibility for VA benefits affect HSA eligibility?

Compliance Team Response:

Special Rule: VA Eligibility Not Disqualifying Coverage

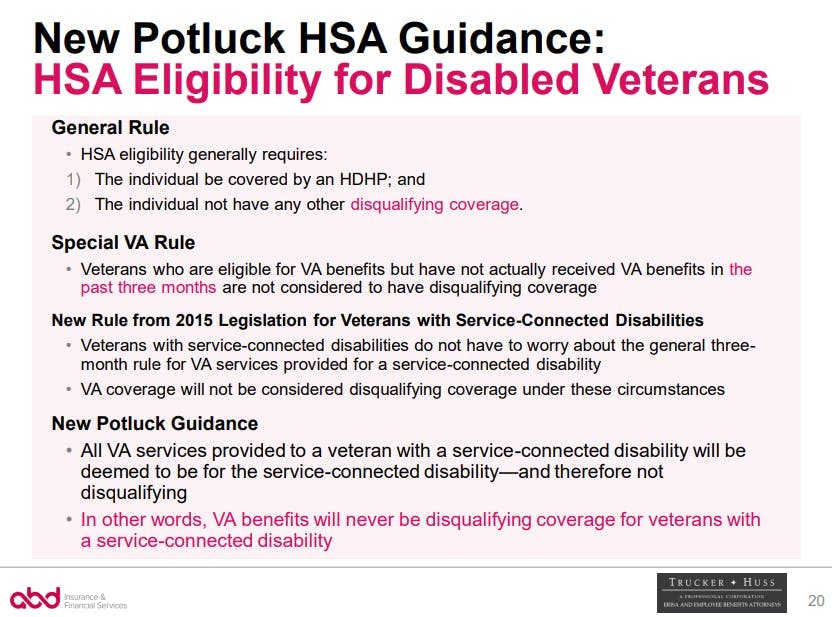

The IRS’s special rule for veterans provides that mere eligibility for VA benefits is not disqualifying coverage for purposes of HSA eligibility—despite the fact that VA benefits are not subject to the minimum HDHP deductible. This is a sharp contrast from the general rule that any pre-deductible coverage blocks HSA eligibility.

This special rule prevents nearly the entire veteran population from being blocked from making or receiving HSA contributions because of their ability to access VA services. However, as described below, veterans who access VA benefits do lose HSA eligibility.

Veterans Who Access VA Benefits: Three-Month Block

Veterans who actually receive medical benefits from the VA do lose HSA eligibility. The IRS rules provide that individuals are not HSA eligible if they received medical benefits from the VA at any time during the previous three months.

Again, veterans must actually access VA benefits for this three-month block on HSA eligibility to apply. Mere eligibility for VA benefits is not disqualifying coverage.

Veterans with Service-Connected Disabilities: Three-Month Rule Does Not Apply

In 2015, Congress passed a new law designed to enhance HSA eligibility for veterans with service-connected disabilities. The modification permits veterans enrolled in a HDHP (with no other disqualifying coverage) and who have a service-connected disability to make or receive HSA contributions regardless of if or when they received VA benefits.

In other words, veterans with a service-connected disability are not blocked from HSA eligibility even if they accessed VA benefits in the prior three months.

Subsequent guidance from the IRS (typically referred to as the “ACA Potluck Guidance”) has confirmed that all VA services provided to a veteran with a service-connected disability are deemed to be provided for the veteran’s service-connected disability. This means that VA benefits will never be disqualifying coverage for veterans with a service-connected disability—even if the VA services are unrelated to the veteran’s service-connected disability.

Regulations

ACA Office Hours: The IRS ACA Potluck Guidance:

Q-5. If an otherwise eligible individual under section 223(c)(1) is eligible for medical benefits through the Department of Veterans Affairs (VA), may he or she contribute to an HSA?

A-5. An otherwise eligible individual who is eligible to receive VA medical benefits, but who has not actually received such benefits during the preceding three months, is an eligible individual under section 223(c)(1). An individual is not eligible to make HSA contributions for any month, however, if the individual has received medical benefits from the VA at any time during the previous three months.

IRS Notice 2015-87, Q/A-20:

https://www.irs.gov/pub/irs-drop/n-15-87.pdf

Question 20: Notice 2004-50, 2004-2 C.B. 196, Q&A-5 provides guidance on the eligibility to contribute to an HSA of an individual who is eligible to receive medical benefits administered by the Department of Veterans Affairs (VA), stating that the individual is not eligible to make HSA contributions for any month if the individual has received medical benefits from the VA at any time during the previous three months. Notice 2008-59, 2008-29 IRB 123, Q&A-9 clarified that although an individual actually receiving medical benefits from the VA at any time in the previous three months generally is not eligible to contribute to an HSA, the disqualification rule does not apply if the medical benefits consist solely of disregarded coverage or preventive care. Section 4007(b) of the Surface Transportation and Veterans Health Care Choice Improvement Act of 2015 (the Surface Transportation Act) amends § 223 to provide that an individual shall not fail to be treated as an eligible individual for any period merely because the individual receives hospital care or medical services under any law administered by the Secretary of Veterans Affairs for a service-connected disability (within the meaning of § 101(16) of title 38, United States Code).

How does § 4007(b) of the Surface Transportation Act affect the prior guidance on the interaction of the receipt of VA health care and eligibility to contribute to an HSA?

Answer 20: As modified by the legislation, an individual actually receiving medical benefits from the VA is not disallowed from making HSA contributions if the medical benefits consist solely of (1) disregarded coverage, (2) preventive care, or (3) hospital care or medical services under any law administered by the Secretary of Veterans Affairs for service-connected disability (within the meaning of § 101(16) of title 38, United States Code). Distinguishing between services provided by the VA for service-connected disabilities and other types of medical care is administratively complex and burdensome for employers and HSA trustees or custodians. Moreover, as a practical matter, most care provided for veterans who have a disability rating will be such qualifying care. Consequently, as a rule of administrative simplification, for purposes of this rule, any hospital care or medical services received from the VA by a veteran who has a disability rating from the VA may be considered to be hospital care or medical services under a law administered by the Secretary of Veterans Affairs for service-connected disability.

Brian Gilmore

Lead Benefits Counsel, VP, Newfront

Brian Gilmore is the Lead Benefits Counsel at Newfront. He assists clients on a wide variety of employee benefits compliance issues. The primary areas of his practice include ERISA, ACA, COBRA, HIPAA, Section 125 Cafeteria Plans, and 401(k) plans. Brian also presents regularly at trade events and in webinars on current hot topics in employee benefits law.

Connect on LinkedIn