HSA Mistaken Contributions

By Brian Gilmore | Published July 31, 2020

**Question: **When can an employer have mistaken HSA contributions returned by the HSA custodian?

**Short Answer: **Although the general rule is that all employer HSA contributions are nonforfeitable, there are three situations that permit employers to correct an error by requesting the HSA custodian return mistaken contributions.

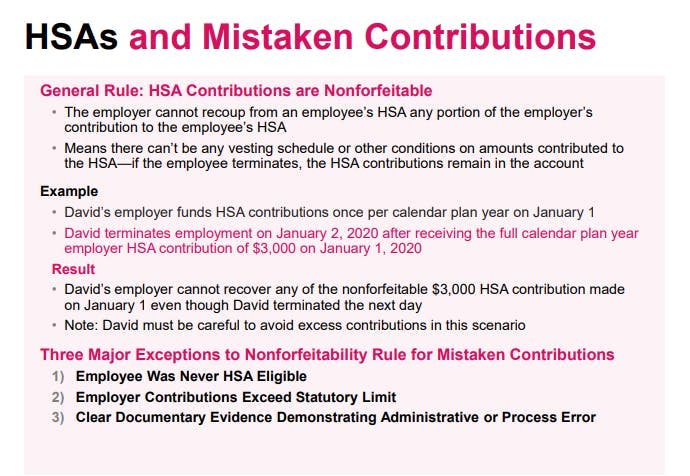

General Rule: HSA Contributions are Nonforfeitable

The general rule is that an employer cannot recoup any portion of its contributions to the employee’s HSA.

This means there can’t be any vesting schedule or other conditions on amounts contributed to the HSA. If an employee terminates, the HSA contributions will always remain in the employee’s account with no opportunity for the employer to have those funds returned.

Example 1:

David’s employer funds HSA contributions once per calendar year on January 1.

David terminates employment on January 2, 2020 after receiving the full calendar plan year employer HSA contribution of $3,000 on January 1, 2020.

Result 1:

David’s employer cannot recover any of the nonforfeitable $3,000 HSA contribution made on January 1—even though David terminated employment the next day.

Note: David must be careful to avoid excess contributions in this situation.

For full details, see our Newfront Go All the Way With HSA Guide.

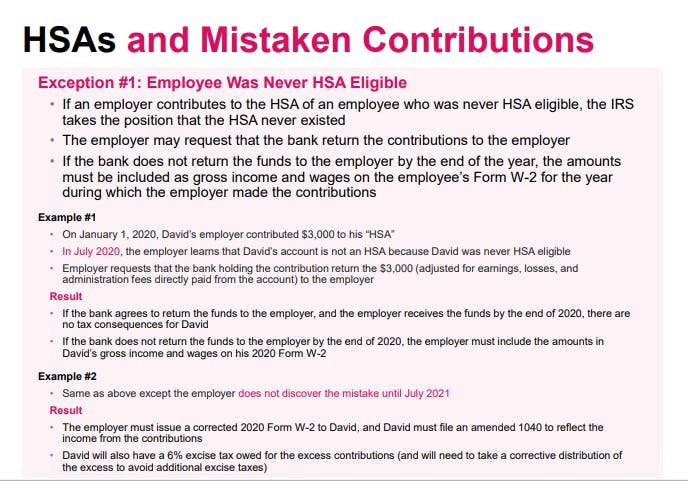

Mistaken Contribution Exception #1: Employee Was Never HSA-Eligible

If an employer contributes to the HSA of an employee who was never HSA-eligible, the IRS takes the position that the HSA never actually existed because it was not properly established. In that case, the employer can correct the error before the end of the calendar year by requesting that the HSA custodian return the contributions (adjusted for earnings and administrative fees) back to the employer.

Assuming the custodian agrees to return the funds, the employer should process the correction as follows:

Mistaken Employer Contributions: Retained by the employer;

Mistaken Employee Contributions: Returned to the employee as taxable income subject to withholding and payroll taxes.

Note that this correction method is available only if the employee was never HSA-eligible (or at least was not HSA-eligible during the year at issue—it is not clear if a period of HSA eligibility prior to the calendar year of the mistaken contribution affects the ability to correct under this method). In other words, if the contributions were mistaken because the employee lost HSA eligibility mid-year, the contributions remain nonforfeitable. In that case, any appropriate correction to address excess contributions would be exclusively a matter for the employee dealing directly with the HSA custodian.

If the employer fails to recover the contributions from the custodian by the end of the calendar year, the contributions will needed to be included as gross income on the employee’s Form W-2 for the year in which the employer made the contributions. This may require the employer to issue a corrected Form W-2c to the employee. Furthermore, the employee would need to take a corrective distribution of the funds by the tax filing deadline (generally April 15 without extension) to avoid a 6% excise tax owed.

Example 2:

On January 1, 2020, Sarah’s employer contributed $3,000 to her “HSA” despite not enrolling in the HDHP.

$2,000 of the contributions were employer contributions, $1,000 of the contributions were employee pre-tax contributions through payroll.

In July 2020, the employer learns that Sarah’s account is not an HSA because Sarah was never HSA-eligible.

The employer requests that the HSA custodian holding the contribution return the $3,000 (adjusted for earnings plus administrative fees) to the employer.

The custodian agrees to the return the funds to the employer, and the employer receives the funds back by the end of 2020.

Result 2:

The employer retains the $2,000 in mistaken employer contributions with no tax consequences to Sarah.

The employer refunds the $1,000 in mistaken employee contributions to Sarah as standard taxable income subject to withholding and payroll taxes.

Example 3:

Same as Example 2, but Sarah’s employer does not discover the error until March 2021.

Result 3:

The employer must issue a corrected 2020 Form W-2c to Sarah to include the mistaken contributions in Sarah’s gross income.

If Sarah already filed her individual return, she will need to file an amended return (generally via Form 1040X) to report the additional income.

Sarah will also need to work directly with the HSA custodian to take a corrective distribution of the full $3,000 by her tax filing deadline (generally April 15 without extensions) to avoid a 6% excise tax on the mistaken contributions.

The employer has no ability to recoup its mistaken contributions in this scenario.

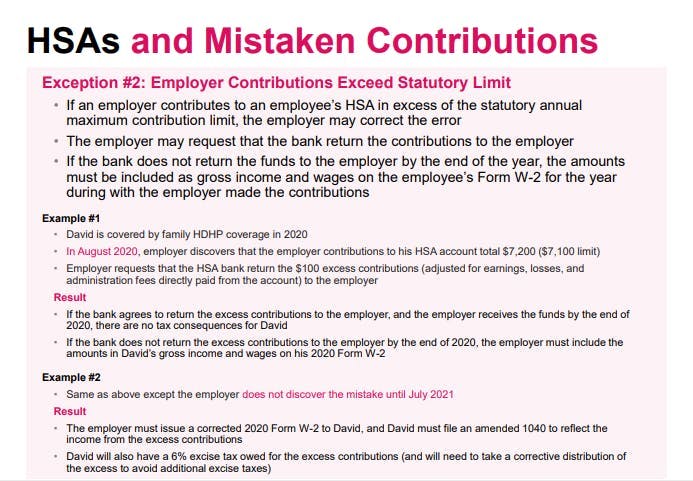

**Mistaken Contribution Exception #2: **Employer Contributions Exceed Statutory Limit

If an employer contributes to an employee’s HSA in excess of the statutory annual maximum contribution limit, the employer may correct the error. In that case, the employer can correct the error before the end of the calendar year by requesting that the HSA custodian return the excess contributions (adjusted for earnings and administrative fees) back to the employer.

Assuming the custodian agrees to return the excess funds, the employer should process the correction as follows:

Excess Employer Contributions: Retained by the employer;

Excess Employee Contributions: Returned to the employee as taxable income subject to withholding and payroll taxes.

Note that this correction method is available only if the contributions exceeded the statutory annual maximum contribution limit. It is not available where the amounts contributed were less than or equal to that limit.

If the employer fails to recover the excess contributions from the custodian by the end of the calendar year, the excess contributions will needed to be included as gross income on the employee’s Form W-2 for the year in which the employer made the contributions. This may require the employer to issue a corrected Form W-2c to the employee. Furthermore, the employee would need to take a corrective distribution of the excess funds by the tax filing deadline (generally April 15 without extension) to avoid a 6% excise tax owed on the excess contributions.

For more details, see our previous post: Excess HSA Contributions.

Example 4:

Tiffany has family HDHP coverage in 2020.

In December 2020, Tiffany’s employer discovers that the employer contributions to her HSA total ,$7200 ($7,100 limit) due to a mistaken excess 00 employer contribution.

$3,100 of the contributions were employer contributions, $4,100 of the contributions were employee pre-tax contributions through payroll.

The employer requests that the HSA custodian return the $100 excess contributions (adjusted for earnings plus administrative fees) to the employer.

The custodian agrees to return the funds to the employer, and the employer receives the funds back by the end of 2020.

Result 4:

The employer retains the $100 in mistaken employer contributions with no tax consequences to Tiffany.

Example 5:

Same as Example 4, but Tiffany’s employer does not discover the error until March 2021.

Result 5:

The employer must issue a corrected 2020 Form W-2c to Tiffany to include the mistaken contributions in Tiffany’s gross income.

If Tiffany already filed her individual return, she will need to file an amended return (generally via Form 1040X) to report the additional income.

Tiffany will also need to work directly with the HSA custodian to take a corrective distribution of the $100 excess contributions by her tax filing deadline (generally April 15 without extensions) to avoid a 6% excise tax on the excess contributions.

The employer has no ability to recoup its excess contributions in this scenario.

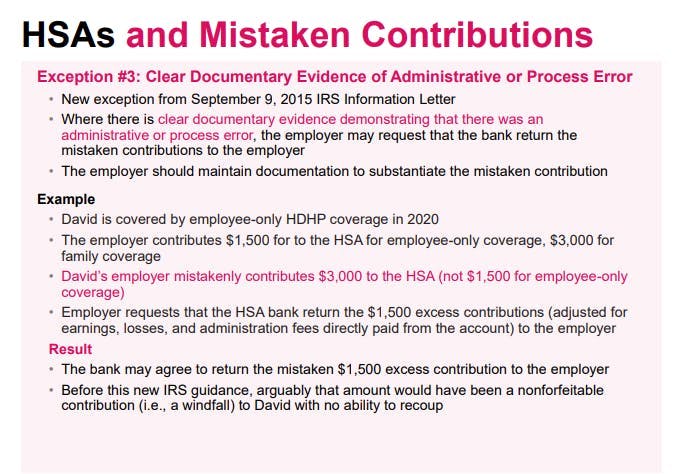

**Mistaken Contribution Exception #3:**Clear Documentary Evidence of an Administrative or Process Error

This third exception is relatively new, deriving from a 2015 IRS Information Letter. It provides that where there is clear documentary evidence demonstrating that there was an administrative or process error, employer can correct the error by requesting that the HSA custodian return the mistaken contributions (adjusted for earnings and administrative fees) back to the employer. In this situation, the employer should maintain the documentation to support its position that a mistaken contribution occurred.

Assuming the custodian agrees to return the mistaken contributions, the employer should process the correction as follows:

Mistaken Employer Contributions: Retained by the employer;

Mistaken Employee Contributions: Returned to the employee as taxable income subject to withholding and payroll taxes.

Unlike the previous two exceptions, it is not clear whether employers may request a refund of mistaken contributions for a prior-year error. That option seems unlikely given that it would generally require a corrected Form W-2c be issued to the employee, and the new IRS guidance does not directly address the issue.

Some examples of situations in which this exception may apply include:

An amount withheld and deposited in an employee’s HSA for a pay period that is greater than the amount shown on the employee’s HSA salary reduction election.

An amount that an employee receives as an employer contribution that the employer did not intend to contribute but was transmitted because an incorrect spreadsheet is accessed or because employees with similar names are confused with each other.

An amount that an employee receives as an HSA contribution because it is incorrectly entered by a payroll administrator (whether in-house or third-party) causing the incorrect amount to be withheld and contributed.

An amount that an employee receives as a second HSA contribution because duplicate payroll files are transmitted.

An amount that an employee receives as an HSA contribution because a change in employee payroll elections is not processed timely so that amounts withheld and contributed are greater than (or less than) the employee elected.

An amount that an employee receives because an HSA contribution amount is calculated incorrectly, such as a case in which an employee elects a total amount for the year that is allocated by the system over an incorrect number of pay periods.

An amount that an employee receives as an HSA contribution because the decimal position is set incorrectly resulting in a contribution greater than intended.

Example 6:

Eric has employee-only HDHP coverage in 2020.

The employer’s policy is to make a $1,500 employer HSA contribution for employees enrolled in employee-only coverage, and a $1,000 employer HSA contribution for employees enrolled in family coverage.

Eric’s employer mistakenly contributes $3,000 to his HSA (not $3,500 for employee-only coverage as intended per its policy).

The employer requests that the HSA custodian return the $3,500 in mistaken contributions (adjusted for earnings plus administrative fees) to the employer.

The custodian agrees to return the funds to the employer, and the employer receives the funds back by the end of 2020.

Result 6:

The employer retains the $1,500 in mistaken employer contributions with no tax consequences to Eric.

Note: Before this new IRS guidance, arguably that amount would have been a nonforfeitable contribution (i.e., a windfall) to Eric with no employer ability to recoup.

For full details on everything HSA, see our Newfront Go All the Way With HSA Guide.

Regulations

IRC §223(d)(1)(E):

(E) The interest of an individual in the balance in his account is nonforfeitable.

IRS Notice: 2004-50, Q/A-82:

https://www.irs.gov/irb/2004-33_IRB#NOT-2004-50

Q-82. May the employer recoup from an employee’s HSA any portion of the employer’s contribution to the employee’s HSA?

A-82. No. Under section 223(d)(1)(E), an account beneficiary’s interest in an HSA is nonforfeitable. For example, on January 2, 2005, the employer makes the maximum annual contribution to employees’ HSAs, in the expectation that the employees would work for the entire calendar year 2005. On February 1, 2005, one employee terminates employment. The employer may not recoup from that employee’s HSA any portion of the contribution previously made to the employee’s HSA.

IRS Notice 2008-59, Q/A-23-25:

https://www.irs.gov/irb/2008-29_IRB#NOT-2008-59

Q-23. If an employer contributes to the account of an employee who was never an eligible individual, can the employer recoup the amounts?

A-23. If the employee was never an eligible individual under § 223(c)(1), then no HSA ever existed and the employer may correct the error. At the employer’s option, the employer may request that the financial institution return the amounts to the employer. However, if the employer does not recover the amounts by the end of the taxable year, then the amounts must be included as gross income and wages on the employee’s Form W-2 for the year during which the employer made the contributions.

Example 1. In February 2008, Employer L contributed $500 to an account of Employee M, reasonably believing the account to be an HSA. In July 2008, Employer L first learned that Employee M’s account is not an HSA because Employee M has never been an eligible individual under § 223(c).

Employer L may request that the financial institution holding Employee M’s account return the balance of the account ($500 plus earnings less administration fees directly paid from the account) to Employer L. If Employer L does not receive the balance of the account, Employer L must include the amounts in Employee M’s gross income and wages on his Form W-2 for 2008.

Example 2. The same facts as Example 1, except Employer L first discovers the mistake in July 2009. Employer L issues a corrected 2008 Form W-2 for Employee M, and Employee M files an amended federal income tax return for 2008.

Q-24. If an employer contributes amounts to an employee’s HSA that exceed the maximum annual contribution allowed in § 223(b) due to an error, can the employer recoup the excess amounts?

A-24. If the employer contributes amounts to an employee’s HSA that exceed the maximum annual contribution allowed in § 223(b) due to an error, the employer may correct the error. In that case, at the employer’s option, the employer may request that the financial institution return the excess amounts to the employer. Alternatively, if the employer does not recover the amounts, then the amounts must be included as gross income and wages on the employee’s Form W-2 for the year during which the employer made contributions. If, however, amounts contributed are less than or equal to the maximum annual contribution allowed in § 223(b), the employer may not recoup any amount from the employee’s HSA.

Q-25. If an employer contributes to the HSA of an employee who ceases to be an eligible individual during a year, can the employer recoup amounts that the employer contributed after the employee ceased to be an eligible individual?

A-25. No. Employers generally cannot recoup amounts from an HSA other than as discussed above in Q&A-23 and Q&A-24. See Notice 2004-50, Q&A-82.

Example. Employee N was an eligible individual on January 1, 2008. On April 1, 2008, Employee N is no longer an eligible individual because Employee N’s spouse enrolled in a general purpose health FSA that covers all family members. Employee N first realizes that he is no longer eligible on July 17, 2008, at which time Employee N informs Employer O to cease HSA contributions.

Employer O’s contributions into Employee N’s HSA between April 1, 2008 and July 17, 2008 cannot be recouped by Employer O because Employee N has a nonforfeitable interest in his HSA. Employee N is responsible for determining if the contributions exceed the maximum annual contribution limit in § 223(b), and for withdrawing the excess contribution and the income attributable to the excess contribution and including both in gross income.

IRS Information Letter 2018-0033:

https://www.irs.gov/pub/irs-wd/18-0033.pdf

Notice 2008-59 does not specifically address other situations in which contributions to an employee’s HSA are the result of the employer’s or trustee’s administrative or process errors, but the notice also was not intended to provide an exclusive set of circumstances in which an employer may request the return of contributed amounts. Rather if there is clear documentary evidence demonstrating that there was an administrative or process error, an employer may request that the financial institution return the amounts to the employer, with any correction putting the parties in the same position that they would have been in had the error not occurred. Employers should maintain documentation to support their assertion that a mistaken contribution occurred.

Outside of the specific situations described in Notice 2008-59, some examples of the type of errors which may be corrected under the standard described above include:

An amount withheld and deposited in an employee’s HSA for a pay period that is greater than the amount shown on the employee’s HSA salary reduction election.

An amount that an employee receives as an employer contribution that the employer did not intend to contribute but was transmitted because an incorrect spreadsheet is accessed or because employees with similar names are confused with each other.

An amount that an employee receives as an HSA contribution because it is incorrectly entered by a payroll administrator (whether in-house or third-party) causing the incorrect amount to be withheld and contributed.

An amount that an employee receives as a second HSA contribution because duplicate payroll files are transmitted.

An amount that an employee receives as an HSA contribution because a change in employee payroll elections is not processed timely so that amounts withheld and contributed are greater than (or less than) the employee elected.

An amount that an employee receives because an HSA contribution amount is calculated incorrectly, such as a case in which an employee elects a total amount for the year that is allocated by the system over an incorrect number of pay periods.

An amount that an employee receives as an HSA contribution because the decimal position is set incorrectly resulting in a contribution greater than intended.

Newfront Go All the Way With HSA Guide

HSAs and Mistaken Contributions General Rule

HSAs and Mistaken Contributions - Exception 1

HSAs and Mistaken Contributions - Exception 2

HSAs and Mistaken Contributions - Exception 3

Brian Gilmore

Lead Benefits Counsel, VP, Newfront

Brian Gilmore is the Lead Benefits Counsel at Newfront. He assists clients on a wide variety of employee benefits compliance issues. The primary areas of his practice include ERISA, ACA, COBRA, HIPAA, Section 125 Cafeteria Plans, and 401(k) plans. Brian also presents regularly at trade events and in webinars on current hot topics in employee benefits law.

Connect on LinkedIn