HSA Last-Month Rule

By Brian Gilmore | Published March 17, 2017

Determining an employee’s HSA contribution limit following a mid-year election can be tricky.

Question: An employee was hired mid-September last year and enrolled in the HDHP coverage on date of hire. What is his 2016 HSA contribution limit?

Compliance Team Answer:

Standard Rule: Proportional Limit

The general rule is that the employee would have a proportional contribution limit based on the number of months of HSA eligibility in 2016. HSA eligibility is determined as of the first day of each calendar month. Even though the employee was enrolled in September, he was not HSA-eligible because he was not enrolled on the first day of the month.

This means that the employee was HSA-eligible for three months in 2016 (October, November, December).

His standard HSA contribution limit for 2016 is therefore 3/12 (1/4) of the statutory limit.

Employee-only coverage: $3,350 x 0.25 = $837.50

Family coverage: $6,750 x. 0.25 = $1,687.50

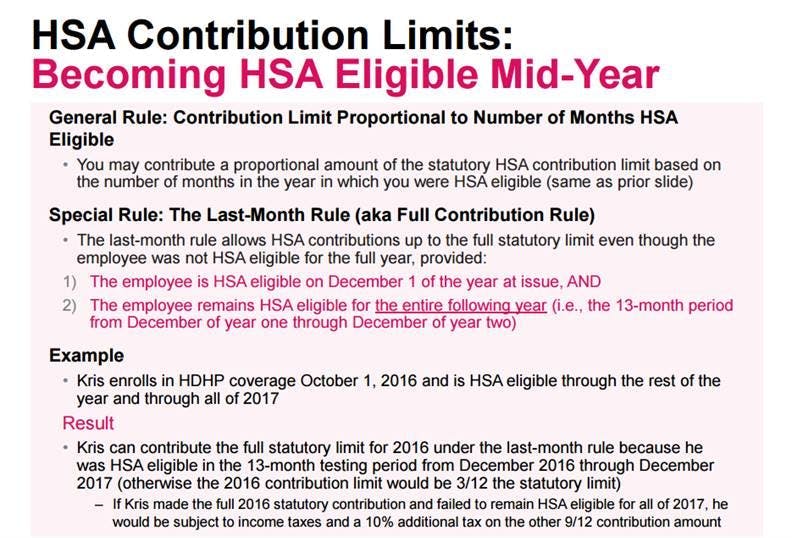

Exception: Full Contribution Under the Last-Month Rule

We find that this rule often confuses employees—so here are three attempts at making sense of this tricky (but useful!) exception.

Regulations:

I. IRS Explanation

IRS Publication 969:

http://www.irs.gov/pub/irs-pdf/p969.pdf

Last-month rule. Under the last-month rule, if you are an eligible individual on the first day of the last month of your tax year (December 1 for most taxpayers), you are considered an eligible individual for the entire year. You are treated as having the same HDHP coverage for the entire year as you had on the first day of the last month.

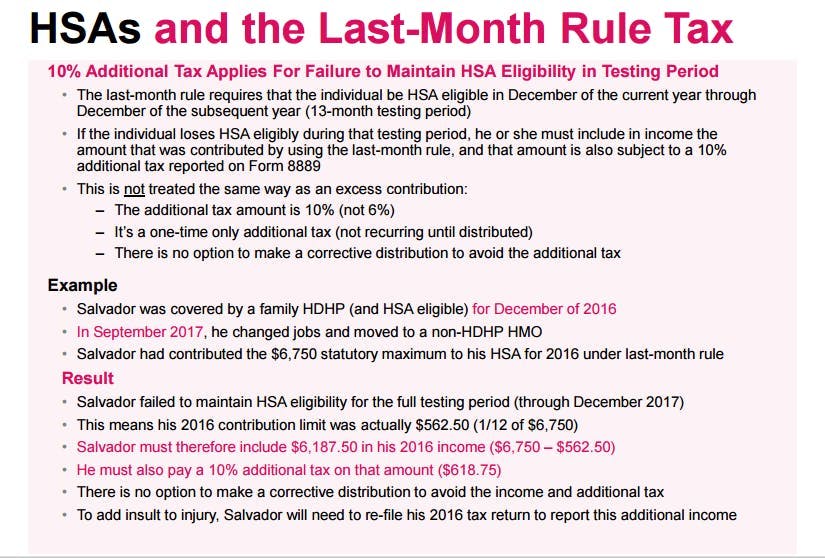

Testing period. If contributions were made to your HSA based on you being an eligible individual for the entire year under the last-month rule, you must remain an eligible individual during the testing period. For the last-month rule, the testing period begins with the last month of your tax year and ends on the last day of the 12th month following that month. For example, December 1, 2015, through December 31, 2016.

If you fail to remain an eligible individual during the testing period, other than because of death or becoming disabled, you will have to include in income the total contributions made to your HSA that would not have been made except for the last-month rule. You include this amount in your income in the year in which you fail to be an eligible individual. This amount is also subject to a 10% additional tax. The income and additional tax are calculated on Form 8889, Part III.

II. Text Explanation

For mid-year HDHP enrollees, the last-month rule will allow HSA contributions up to the full statutory HSA limit even though the employee was not HSA eligible for the full year.

The Catch—In order to qualify for the last-month rule, the employee must:

Be HSA-eligible on December 1 of the year at issue; AND

Remain HSA-eligible for the entire year following the year at issue.

In other words, there is a 13-month “testing period” that applies. You need to be eligible December 1 through the entire subsequent year to contribute the full HSA amount in the year in which you became HSA eligible.

For example: Let’s say employee Bob was a new hire on September 14, 2016. Bob enrolled in the company’s HDHP and become HSA-eligible as of October 1, 2016.

Under the general rule, Bob would be limited to 3/12 (1/4) of the HSA contribution limit for 2016.

Under the last-month rule, Bob can contribute the full $3,350/$6,750 for 2016 as long has he remains HSA-eligible (i.e., enrolled in an HDHP with no disqualifying coverage) on December 1, 2016 and for all of 2017.

If Bob takes advantage of the last-month rule and fails to maintain HSA eligibility through the end of 2017, he will be subject to income taxes and a 10% additional tax on the amount of his excess contributions (9/12 of his contribution).

III. PPT Explanation

HSA Contribution Limits

HSAs and the Last-Month Rule Tax

Brian Gilmore

Lead Benefits Counsel, VP, Newfront

Brian Gilmore is the Lead Benefits Counsel at Newfront. He assists clients on a wide variety of employee benefits compliance issues. The primary areas of his practice include ERISA, ACA, COBRA, HIPAA, Section 125 Cafeteria Plans, and 401(k) plans. Brian also presents regularly at trade events and in webinars on current hot topics in employee benefits law.

Connect on LinkedIn