Health FSA Reimbursements after Termination of Employment

By Brian Gilmore | Published March 10, 2017

This week’s question is a two part question dealing with the regulations surrounding reimbursement of FSA claims after termination of employment and options available.

Question Part I: Does an employee ever have longer than 90 days to submit health FSA claims after terminating employment?

Compliance Team Answer:

Run-Out Period

Cafeteria plans typically provide for a 90-day run-out period to submit FSA claims incurred prior to termination. Check the cafeteria plan document for the FSA to confirm. Although this is the most common structure, it is not legally required. This is purely a matter of plan design.

Note that the cafeteria plan may provide that health FSA coverage (i.e., the ability to incur reimbursable claims) continues through the end of the month in which the employee terminates, similar to many major medical/dental/vision plans. This provision is not common for the health FSA, but it is permitted. In the case where coverage continues through the end of the month, the 90-day run-out period will begin as of the end of the month.

COBRA

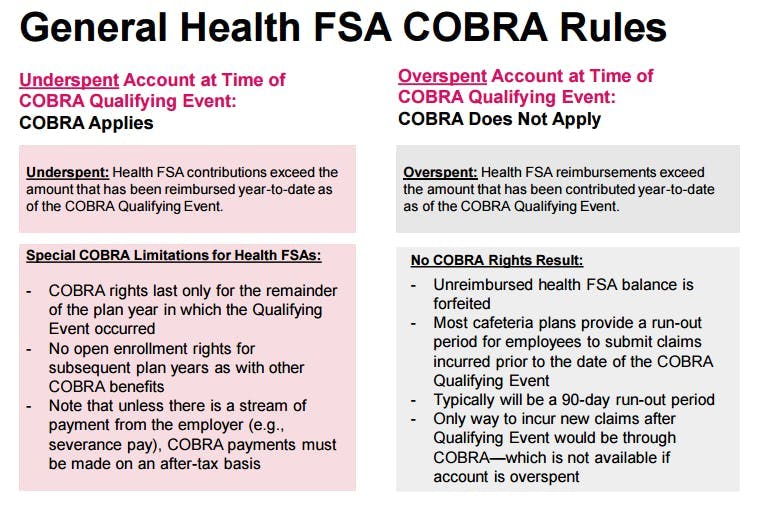

Underspent health FSA accounts generally can be continued through COBRA until the end of the plan year in which the employee terminates. COBRA permits an employee to incur reimbursable claims through the end of the plan year in which the employee terminates (i.e., remain “covered” by the health FSA for the remainder of the plan year).

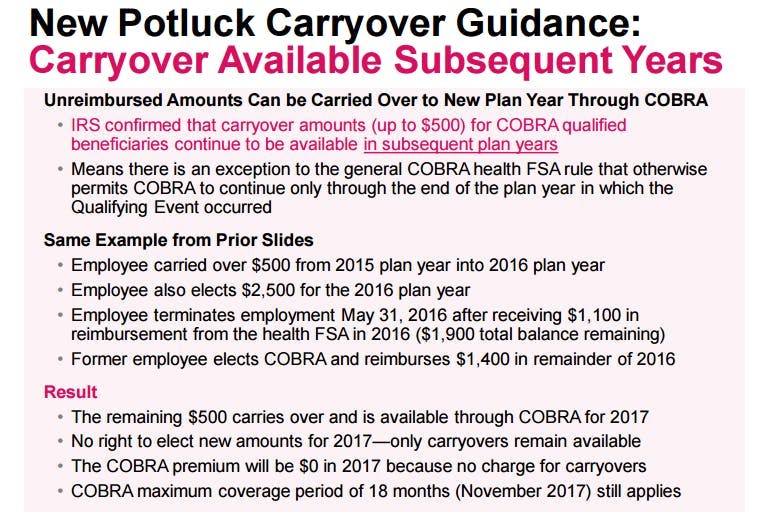

Note that if the plan offers the carryover provision, up to $500 of the unused amount may carry over to the subsequent plan year for the COBRA maximum coverage period (18 months from the termination of employment).

Summary of Options to Provide to Employee

The company’s health FSA is a component of company’s cafeteria plan, which is governed by Internal Revenue Code §125. The Section 125 regulations provide that company must follow the written terms of its cafeteria plan document to maintain the tax-advantaged status of employees’ health FSA elections.

Upon terminating employment, you lost coverage under the company’s health FSA. However, there are two options available to you to address unreimbursed funds remaining in the company’s health FSA at the time of your termination:

Run-Out Period: The company’s cafeteria plan provides a 90-day run-out period [WE NEED TO CONFIRM FIRST IN PLAN DOC] for terminated employees to submit claims incurred prior to termination. You must follow the plan’s procedures to properly submit any outstanding claims within that run-out period. At the end of the run-out period, the use-it-or-lose-it rule for health FSAs requires that any unreimbursed funds be forfeited to the plan unless you elect COBRA (see #2).

COBRA: Upon terminating from employment, you experienced a COBRA qualifying event to continue coverage under the company’s health FSA through the end of the plan year. This option will be available to you only if your account was underspent at the time of termination (i.e., you had contributed more than you had been reimbursed at the time of the qualifying event). If you timely elect and pay for COBRA continuation coverage under the health FSA, you will be able to continue incurring claims for reimbursement through the end of the plan year. Up to $500 remaining in your health FSA at the end of the plan year will be subject to the plan’s carryover provision and may continue to be available for the duration of your maximum COBRA period (18 months from termination). [DELETE IF THE PLAN DOES NOT OFFER CARRYOVER]

Question Part II: Can we permit any exceptions or refunds?

Compliance Team Answer:

Section 125 Use-It-Or-Lose-It Rule

The health and dependent care FSAs are components of the company’s Section 125 cafeteria plan. Internal Revenue Code §125 (and its implementing regulations) imposes very strict limitations on the administration of cafeteria plans. One of the most fundamental of these limitations is that all FSA elections are subject to the use-it-or-lose-it rule. This means that after the end of the plan year (or earlier termination of employment) and any grace and/or run-out period, any remaining unreimbursed funds not subject to a carryover provision must be forfeited to the plan.

Plan Disqualification Risk

Unfortunately, there is no option for employers to make exceptions to these rules or refund to employees any unreimbursed FSA amounts remaining at the end of the plan year (plus any related grace period and/or run-out period) or after the run-out period following termination of employment. Engaging in this practice would risk disqualifying the entire Section 125 cafeteria plan if discovered by the IRS, resulting in all elections becoming taxable to all employees.

Permitted Use of Experience Gains from Forfeitures

The Section 125 regulations provide the following permitted plan uses of experience gains resulting from forfeitures:

(A) To reduce required salary reduction amounts for the immediately following plan year, on a reasonable and uniform basis, as described in paragraph (o)(2) of this section;

(B) Returned to the employees on a reasonable and uniform basis, as described in paragraph (o)(2) of this section; or

(C) To defray expenses to administer the cafeteria plan.

Refunding the employee for the remaining unspent amount is not permitted. As a practical matter, employers almost always apply experience gains from forfeitures to the health FSA’s plan administrative expenses.

Keep in mind that experience gains are the result of annual forfeitures reduced by the health FSA’s losses from overspent accounts by employees who terminate mid-year. The experience gains (if any) might be significantly lower than the gross forfeiture amount if there were a lot of mid-year terminations with overspent accounts.

Amending the Plan Run-Out Period

Lastly, it is possible to amend the company’s Section 125 cafeteria plan to permit a run-out period longer than 90 days for all participants (the run-out period must be consistent for all). That is very unusual, and it would need to be coordinated with the TPA, but it could be done.

However, keep in mind that Section 125 requires that all plan amendments be prospective in effect only. This means that any amendment could not affect the current situation (it would only apply going forward).

General Health FSA COBRA Rules

COBRA Carryover Guidance

Prop. Treas. Reg. §1.125-5(c):

(c) Use-or-lose rule.

(1) In general. An FSA may not defer compensation. No contribution or benefit from an FSA may be carried over to any subsequent plan year or period of coverage. See paragraph (k)(3) in this section for specific exceptions. Unused benefits or contributions remaining at the end of the plan year (or at the end of a grace period, if applicable) are forfeited.

Prop. Treas. Reg. §1.125-1(c)(7):

(7) Operational failure.

(i) In general. If the cafeteria plan fails to operate according to its written plan or otherwise fails to operate in compliance with section 125 and the regulations, the plan is not a cafeteria plan and employees’ elections between taxable and nontaxable benefits result in gross income to the employees.

(ii) Failure to operate according to written cafeteria plan or section 125. Examples of failures resulting in section 125 not applying to a plan include the following—

(A) Paying or reimbursing expenses for qualified benefits incurred before the later of the adoption date or effective date of the cafeteria plan, before the beginning of a period of coverage or before the later of the date of adoption or effective date of a plan amendment adding a new benefit;

(B) Offering benefits other than permitted taxable benefits and qualified benefits;

(C) Operating to defer compensation (except as permitted in paragraph (o) of this section);

(D) Failing to comply with the uniform coverage rule in paragraph (d) in §1.125-5;

(E) Failing to comply with the use-or-lose rule in paragraph (c) in §1.125-5;

(F) Allowing employees to revoke elections or make new elections, except as provided in §1.125-4 and paragraph (a) in §1.125-2;

(G) Failing to comply with the substantiation requirements of § 1.125-6;

(H) Paying or reimbursing expenses in an FSA other than expenses expressly permitted in paragraph (h) in §1.125-5;

(I) Allocating experience gains other than as expressly permitted in paragraph (o) in §1.125-5;

(J) Failing to comply with the grace period rules in paragraph (e) of this section; or

(K) Failing to comply with the qualified HSA distribution rules in paragraph (n) in §1.125-5.

Prop. Treas. Reg. §1.125-1(f):

(f) Run-out period. A cafeteria plan is permitted to contain a run-out period as designated by the employer. A run-out period is a period after the end of the plan year (or grace period) during which a participant can submit a claim for reimbursement for a qualified benefit incurred during the plan year (or grace period). Thus, a plan is also permitted to provide a deadline on or after the end of the plan year (or grace period) for submitting a claim for reimbursement for the plan year. Any run-out period must be provided on a uniform and consistent basis with respect to all participants.

Prop. Treas. Reg. §1.125-5(o):

(o) FSA experience gains or forfeitures.

(1) Experience gains in general. An FSA experience gain (sometimes referred to as forfeitures in the use-or-lose rule in paragraph (c) in this section) with respect to a plan year (plus any grace period following the end of a plan year described in paragraph (e) in §1.125-1), equals the amount of the employer contributions, including salary reduction contributions, and after-tax employee contributions to the FSA minus the FSA’s total claims reimbursements for the year. Experience gains (or forfeitures) may be—

(i) Retained by the employer maintaining the cafeteria plan; or

(ii) If not retained by the employer, may be used only in one or more of the following ways—

(A) To reduce required salary reduction amounts for the immediately following plan year, on a reasonable and uniform basis, as described in paragraph (o)(2) of this section;

(B) Returned to the employees on a reasonable and uniform basis, as described in paragraph (o)(2) of this section; or

(C) To defray expenses to administer the cafeteria plan.

(2) Allocating experience gains among employees on reasonable and uniform basis. If not retained by the employer or used to defray expenses of administering the plan, the experience gains must be allocated among employees on a reasonable and uniform basis. It is permissible to allocate these amounts based on the different coverage levels of employees under the FSA. Experience gains allocated in compliance with this paragraph (o) are not a deferral of the receipt of compensation. However, in no case may the experience gains be allocated among employees based (directly or indirectly) on their individual claims experience. Experience gains may not be used as contributions directly or indirectly to any deferred compensation benefit plan.

Prop. Treas. Reg. §1.125-1(c)(5):

(5) Amendments to cafeteria plan. Any amendment to the cafeteria plan must be in writing. A cafeteria plan is permitted to be amended at any time during a plan year. However, the amendment is only permitted to be effective for periods after the later of the adoption date or effective date of the amendment. For an amendment adding a new benefit, the cafeteria plan must pay or reimburse only those expenses for new benefits incurred after the later of the amendment’s adoption date or effective date.

Brian Gilmore

Lead Benefits Counsel, VP, Newfront

Brian Gilmore is the Lead Benefits Counsel at Newfront. He assists clients on a wide variety of employee benefits compliance issues. The primary areas of his practice include ERISA, ACA, COBRA, HIPAA, Section 125 Cafeteria Plans, and 401(k) plans. Brian also presents regularly at trade events and in webinars on current hot topics in employee benefits law.

Connect on LinkedIn