Group-Term Life - Imputed Income

By Brian Gilmore | Published April 10, 2020

Question: What are the imputed income requirements for employer-sponsored group-term life coverage?

Short Answer: Employers must include the value of group-term life coverage in excess of $50,000 in employees’ taxable income.

General Rule: Imputed Income for GTL Coverage in Excess of $50,000

Internal Revenue Code 79 provides for an exclusion from income for group-term life (GTL) premiums only up to $50,000 in coverage. This means that any employer-provided GTL coverage in excess of $50,000 will result in imputed income to the employee.

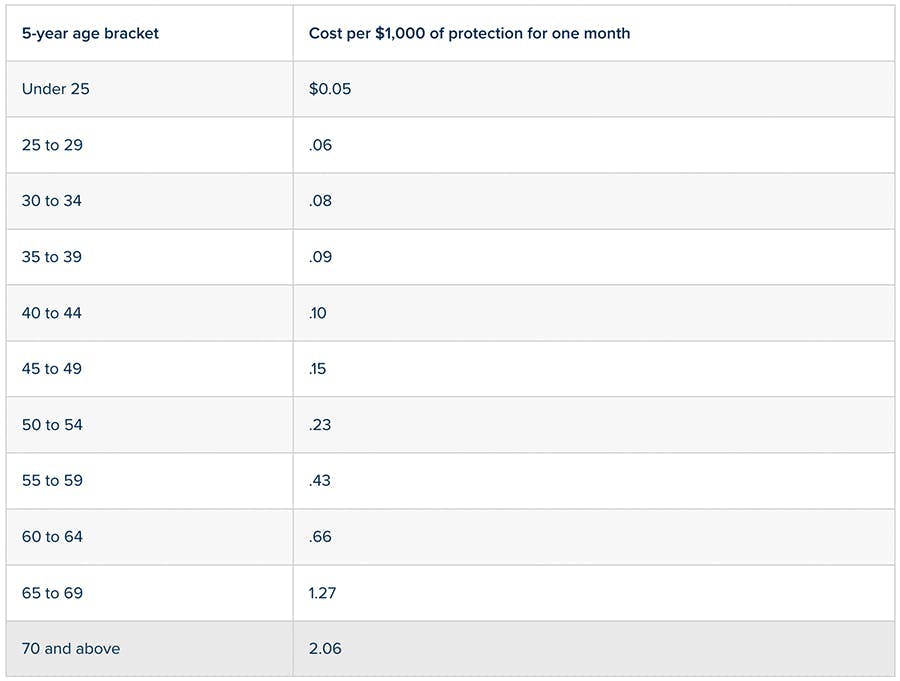

The amount of the imputed income varies by age based on the IRS Table I rates:

Employers must impute income for the entire year based on the employee’s age on the last day of the calendar year. These imputed income amounts are typically built into the employer’s payroll system and can be automated for ease of administration.

Example:

An employee who will reach age 50 by the end of the calendar year has $175,000 in GTL coverage paid for by the employer.

Result:

There is $125,000 in “excess coverage” (i.e., GTL coverage in excess of $50,000) that is subject to imputed income.

The employee would therefore be subject to imputed income of 125 (excess coverage units) x $0.23 (Table I rate for age 50) x 12 (months) = $345/year.

GTL Imputed Income Payroll Procedures

The following is a list of more specific procedural issues related to GTL imputed income:

The employer must report the GTL imputed income by the pay period, by the quarter, or on any other basis (e.g., annual) as long as the reporting is done at least once per year.

No formal choice on the interval is required (i.e., there is no requirement to inform the IRS of the interval, and the employer can change its approach at any time and for any reason).

The reporting must be included by December 31 of each year.

The GTL imputed income is not subject to income tax withholding or FUTA withholding.

The GTL imputed income is subject to FICA payroll taxes and withholding.

Employers may choose to gross up employees on the tax liability caused by the GTL imputed income as they see fit.

GTL imputed income is reported on the Form W-2 as wages (Box 1), SS wages (Box 3), Medicare wages (Box 5), and in Box 12 using Code “C”.

GTL Opt-Out Procedures

Even though employees are not required to contribute employer-provided basic GTL coverage (as opposed to employee-paid voluntary life coverage), some employees may want to opt-out of the benefit to avoid the imputed income amounts.

There is no requirement to permit an employee opt-out from the employer-paid basic GTL because there are no employee contributions. However, most employers do permit employees to waive the coverage if the employee requests it. The GTL carrier will generally permit the opt-out because it is rare that employees request it. Best practice is to have employees complete a GTL benefit opt-out form in these circumstances.

Alternatives to Avoid GTL Imputed Income

Other than waiving the GTL benefit, there are a couple alternatives available to employers and employees to avoid the GTL imputed income:

The employer could gross up the employee for the tax liability caused by the GTL coverage in excess of $50k.

The employee could designate a charity as the sole beneficiary of the policy. That avoids the imputed income on the value of coverage in excess of $50k.

Voluntary GTL Benefits Paid by the Employee

Where the employer-paid basic GTL coverage exceeds $50,000, employees will generally pay the premiums for any additional voluntary coverage on an after-tax basis—because the $50k exclusion from income has already been exhausted by the basic coverage. This avoids the need to impute income on any amount of the additional voluntary GTL coverage purchased by the employee.

If the employer does not offer basic GTL coverage (or offers coverage at an amount lower than $50,000), the employer can permit the employee to pay pre-tax the employee premium for up to $50,000 of voluntary GTL coverage on a pre-tax basis. Any amount in excess $50,000 would generally be paid on an after-tax basis to avoid the need to impute income.

Pre-tax employee GTL premium payments for voluntary GTL coverage in excess of $50,000 (basic and voluntary coverage combined) are subject to imputed income through the Table I chart in the same manner as employer-paid basic GTL coverage in excess of $50,000. Depending on age, this can result in significantly higher tax liability for the employee than simple after-tax premium payments for voluntary coverage in excess of $50,000. Therefore, most employers have structured payroll provide that employees pay for voluntary GTL coverage in excess of $50,000 (basic and voluntary combined) exclusively on an after-tax basis.

Spouse/Dependent GTL Coverage

GTL insurance for a spouse or dependent is excludible from the employee’s income only if the coverage amount is $2,000 or less. The IRS deems this low level of coverage to qualify as a de minim is fringe benefit.

Spouse or dependent GTL coverage in excess of $2,000 paid by the employer is subject to imputed income at the standard Table I rates. The full amount is taxable (i.e., not simply the coverage in excess of $2,000), and income tax withholding applies (unlike imputed income for employee GTL coverage). Voluntary spouse or dependent GTL coverage in excess of $2,000 should be paid by the employee on an after-tax basis and therefore not subject to imputed income.

Partial Month Coverage Prorated Imputed Income

IRS guidance states that employers should prorate the cost from Table I if less than a full month of coverage is involved. Nonetheless, we generally do not see any issues with taking a full month’s imputed income amount even for a mid-month hire or termination where GTL coverage is only a partial month. That appears to be the more common approach in practice.

For more details, see our previous post: Final Paycheck Issues.

Potential Penalties

The primary potential penalty for failure to correctly impute GTL income is the Form W-2 penalties for incorrectly reporting income.

Those Form W-2 penalties are generally as follows:

$50 per Form W-2 if corrected within 30 days of the 1/31 due date ($556,500 annual maximum, reduced to $194,500 for small business)

$110 per Form W-2 if corrected after 30 days, but no later than August 1 ($1,669,500 annual maximum, reduced to $556,500 for small business)

$270 per Form W-2 if corrected after August 1 or not corrected ($3,339,000 annual maximum, reduced to $1,113,000 for small business)

$550+ per form W-2 if due to intentional disregard of the Form W-2 requirements (no annual maximum)

Note that these penalties apply once for the incorrect filing with the IRS, and once for the incorrect furnishing to employees. So they are generally doubled in practice. Corrections are generally reported via IRS Form W-2c.

Other Posts Addressing Group-Term Life Plans

For more details on employer-sponsored GTL coverage:

Regulations

Treas. Reg. 1.79-3(b)(1):

(b) Determination of the portion of the group-term life insurance on the employee’s life to be taken into account.

_(1) _For each “period of coverage” (as defined in paragraph (c) of this section), the portion of the group-term life insurance to be taken into account in computing the amount includible in an employee’s gross income for purposes of paragraph (a)(1) of this section is the sum of the proceeds payable upon the death of the employee under each policy, or portion of a policy, of group-term life insurance on such employee’s life to which the rule of inclusion set forth in section 79(a) applies, less $50,000 of such insurance. Thus, the amount of any proceeds payable under a policy, or portion of a policy, which qualifies for one of the exceptions to the rule of inclusion provided by section 79(b) is not taken into account. For the regulations relating to such exceptions to the rule of inclusion, see §1.79-2.

Treas. Reg. 1.79-3(c):

(c) Period of coverage. For purposes of this section, the phrase “period of coverage” means any one calendar month period, or part thereof, during the employee’s taxable year during which the employee is provided group-term life insurance on his life to which the rule of inclusion set forth in section 79(a) applies. The phrase “part thereof” as used in the preceding sentence means any continuous period which is less than the one calendar month period referred to in the preceding sentence for which premiums are charged by the insurer.

Treas. Reg. §1.79-3(d)(2):

_(2) _For the cost of group-term life insurance provided after June 30, 1999, the following table sets forth the cost of ,000 of group-term life insurance provided for one month, computed on the basis of 5-year age brackets. See 26 CFR §1.79-3(d)(2) in effect prior to July 1, 1999, and contained in the 26 CFR part 1 edition revised as of April 1, 1999, for a table setting forth the cost of group-term life insurance provided before July 1, 1999. For purposes of Table I, the age of the employee is the employee’s attained age on the last day of the employee’s taxable year.

Table I. – Uniform Premiums for ,000 of Group-Term Life Insurance Protection

Treas. Reg. 1.79-2(c):

(c) Employer or charity a beneficiary.

_(1) General rule. _Section 79(b)(2) provides an exception with respect to the amounts referred to in section 79(a) for the cost of any portion of the group-term life insurance on the life of an employee provided during part or all of the taxable year of the employee under which the employer is directly or indirectly the beneficiary, or under which a person described in section 170(c) (relating to definition of charitable contributions) is the sole beneficiary, for the entire period during such taxable year for which the employee receives such insurance.

…

(3) Charity a beneficiary.

(i) For purposes of section 79(b)(2) and subparagraph (1) of this paragraph, a person described in section 170(c) is a beneficiary under a policy providing group-term life insurance if such person is designated the beneficiary under the policy by any assignment or designation of beneficiary under the policy which, under the law of the jurisdiction which is applicable to the policy, has the effect of making such person the beneficiary under such policy (whether or not such designation is revocable during the taxable year). Such a designation may be made by the employee with respect to any portion of the group-term life insurance on his life. However, no deduction is allowed under section 170, relating to charitable, etc., contributions and gifts, with respect to any such assignment or designation.

(ii) A person described in section 170(c) must be designated the sole beneficiary under the policy or portion of the policy. Such requirement is satisfied if the person described in section 170(c) is the beneficiary under such policy or portion of the policy, and there is no contingent or similar beneficiary under such policy or such portion other than a person described in section 170(c). A general “preference beneficiary clause” in a policy governing payment where there is no designated beneficiary in existence at the death of the employee will not of itself be considered to create a contingent or similar beneficiary. A person described in section 170(c) may be designated the beneficiary under a portion of the policy if such person is designated the sole beneficiary under a beneficiary designation which is expressed, for example, as a fraction of the amount of insurance on the insured’s life.

(iii) If a person described in section 170(c) is designated under the policy (or portion thereof) and such person remains the beneficiary for the period beginning May 1, 1964, and ending with the close of the first taxable year of the employee ending after April 30, 1964, such person shall be treated as the beneficiary under the policy (or the portion thereof) for the period beginning January 1, 1964, and ending April 30, 1964.

IRS Group-Term Life Insurance:

https://www.irs.gov/government-entities/federal-state-local-governments/group-term-life-insurance

Total Amount of Coverage

IRC section 79 provides an exclusion for the first $50,000 of group-term life insurance coverage provided under a policy carried directly or indirectly by an employer. There are no tax consequences if the total amount of such policies does not exceed $50,000. The imputed cost of coverage in excess of $50,000 must be included in income, using the IRS Premium Table, and are subject to social security and Medicare taxes.

…

Coverage for Spouse and Dependents

The cost of employer-provided group-term life insurance on the life of an employee’s spouse or dependent, paid by the employer, is not taxable to the employee if the face amount of the coverage does not exceed $2,000. This coverage is excluded as a de minimis fringe benefit.

Whether a benefit provided is considered de minimis depends on all the facts and circumstances. In some cases, an amount greater than ,000 of coverage could be considered a de minimis benefit. See Notice 89-110 for more information.

If part of the coverage for a spouse or dependents is taxable, the same Premium Table is used as for the employee. The entire amount is taxable, not just the amount that exceeds $2,000.

IRS Notice 89-110:

https://www.irs.gov/pub/irs-drop/n-89-110.pdf

In addition, effective January 1, 1989, and until further notice, the following rules shall apply under section 132(e) of the Code: (1) if the face amount of employer-provided group-term life insurance payable on the death of a spouse or dependent of an employee does not exceed $2,000, such insurance shall be deemed to be de minimis fringe benefit; and (2) in determining whether employer-provided dependent group-term life insurance with a higher face amount is a de minimis fringe benefit, only the excess (if any) of the cost of such insurance over the amount paid for the insurance by the employee on an after-tax basis shall be taken into account. Finally, section 1.61-2(d)(2)(ii)(b) of the regulations is clarified to provide that the cost of employer-provided dependent group-term life insurance is not includible in gross income under that section of the regulations (regardless of whether section 132(e) of the Code applies) to the extent such cost is paid by the employee on an after-tax basis. For purposes of this paragraph, the cost of insurance shall be determined under section 1.79-3(d)(2) of the regulations.

IRS Publication 15-B:

https://www.irs.gov/pub/irs-pdf/p15b.pdf

Exclusion from wages.

You can generally exclude the cost of up to $50,000 of group-term life insurance coverage from the wages of an insured employee. You can exclude the same amount from the employee’s wages when figuring social security and Medicare taxes. In addition, you don’t have to withhold federal income tax or pay FUTA tax on any group-term life insurance you provide to an employee.

Coverage over the limit.

You must include in your employee’s wages the cost of group-term life insurance beyond $50,000 worth of coverage, reduced by the amount the employee paid toward the insurance. Report it as wages in boxes 1, 3, and 5 of the employee’s Form W-2. Also, show it in box 12 with code “C.” The amount is subject to social security and Medicare taxes, and you may, at your option, withhold federal income tax.

Figure the monthly cost of the insurance to include in the employee’s wages by multiplying the number of thousands of dollars of all insurance coverage over $50,000 (figured to the nearest $100) by the cost shown in Table 2-2. For all coverage provided within the calendar year, use the employee’s age on the last day of the employee’s tax year. You must prorate the cost from the table if less than a full month of coverage is involved.

Example.

Tom’s employer provides him with group-term life insurance coverage of $200,000. Tom is 45 years old, isn’t a key employee, and pays $100 per year toward the cost of the insurance. Tom’s employer must include $170 in his wages. The $200,000 of insurance coverage is reduced by $50,000. The yearly cost of $150,000 of coverage is $270 ($0.15 x 150 x 12), and is reduced by the $100 Tom pays for the insurance. The employer includes $170 in boxes

1, 3, and 5 of Tom’s Form W-2. The employer also enters $170 in box 12 with code “C.”

Coverage for dependents.

Group-term life insurance coverage paid by the employer for the spouse or dependents of an employee may be excludable from income as a de minimis fringe benefit if the face amount isn’t more than $2,000. If the face amount is greater than $2,000, the dependent coverage may be excludable from income as a de minimis fringe benefit if the excess (if any) of the cost of insurance over the amount the employee paid for it on an after-tax basis is so small that accounting for it is unreasonable or administratively impracticable.

IRS Forms W-2 and W-3 Instructions

https://www.irs.gov/pub/irs-pdf/iw2w3.pdf

Failure to file correct information returns by the due date.

If you fail to file a correct Form W-2 by the due date and cannot show reasonable cause, you may be subject to a penalty as provided under section 6721. The penalty applies if you:

Fail to file timely,

Fail to include all information required to be shown on Form W-2,

Include incorrect information on Form W-2,

File on paper forms when you are required to e-file,

Report an incorrect TIN,

Fail to report a TIN, or

Fail to file paper Forms W-2 that are machine readable.

The amount of the penalty is based on when you file the correct Form W-2. Penalties are indexed for inflation. The penalty amounts shown below apply for filings due after December 31, 2019. The penalty is:

$50 per Form W-2 if you correctly file within 30 days of the due date; the maximum penalty is $556,500 per year ($194,500 for small businesses, defined in Small businesses).

$110 per Form W-2 if you correctly file more than 30 days after the due date but by August 1; the maximum penalty is $1,669,500 per year ($556,500 for small businesses).

$270 per Form W-2 if you file after August 1, do not file corrections, or do not file required Forms W-2; the maximum penalty is $3,339,000 per year ($1,113,000 for small businesses).

If you do not file corrections and you do not meet any of the exceptions to the penalty, the penalty is $270 per information return. The maximum penalty is $3,339,000 per year ($1,113,000 for small businesses).

Intentional disregard of filing requirements.

If any failure to timely file a correct Form W-2 is due to intentional disregard of the filing or correct information requirements, the penalty is at least $550 per Form W-2 with no maximum penalty.

Failure to furnish correct payee statements.

If you fail to provide correct payee statements (Forms W-2) to your employees and cannot show reasonable cause, you may be subject to a penalty as provided under section 6722. The penalty applies if you fail to provide the statement by January 31, 2020, if you fail to include all information required to be shown on the statement, or if you include incorrect information on the statement.

The amount of the penalty is based on when you furnish the correct payee statement. This penalty is an additional penalty and is applied in the same manner, and with the same amounts, as in Failure to file correct information returns by the due date.

Brian Gilmore

Lead Benefits Counsel, VP, Newfront

Brian Gilmore is the Lead Benefits Counsel at Newfront. He assists clients on a wide variety of employee benefits compliance issues. The primary areas of his practice include ERISA, ACA, COBRA, HIPAA, Section 125 Cafeteria Plans, and 401(k) plans. Brian also presents regularly at trade events and in webinars on current hot topics in employee benefits law.

Connect on LinkedIn