Employer HSA Contributions during Protected Leave

By Brian Gilmore | Published August 10, 2018

**Question: **Are employers required to continue making the employer HSA contribution for employees on a protected leave of absence?

Compliance Team Response:

As described below, employers are not required to make the employer HSA contribution for employees on a protected leave of absence.

The primary protected leave laws (FMLA and CFRA/PDL, or other state equivalents) require employers to maintain employer-sponsored group health plan benefits for an employee on protected leave. Coverage must continue to be available on the same conditions as if the employee were actively at work. Employees on these forms of protected leave therefore have the right to continue active (i.e., not COBRA) health plan coverage by paying the same employee-share of the premium as an active employee (i.e., the employer must continue to contribute the standard employer-share of the premium).

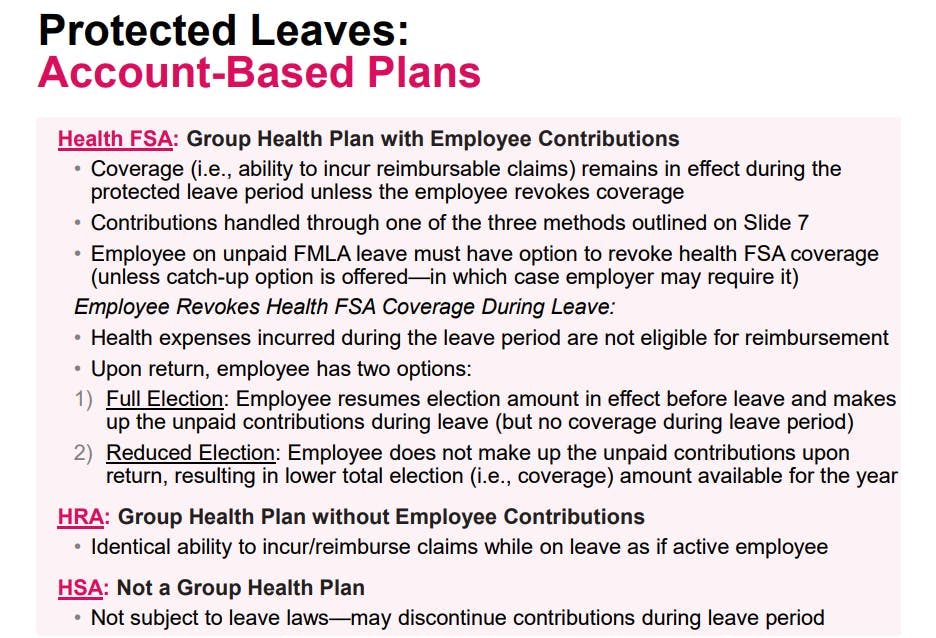

However, HSAs are not an employer-sponsored plan. An HSA is a personal trust/custodial account controlled solely by the employee, and it is therefore not subject to ERISA as a group health plan. The employer may contribute to the HSA of employees enrolled in an HDHP and who open a HSA with the employer’s preferred custodian (as is the case here), but the HSA itself is not the employer’s plan.

Because the HSA is not an employer-sponsored group health plan, the employer has no obligation to continue making contributions to the account while an employee is on protected leave.

The default approach is therefore to discontinue employer HSA contributions for an employee on protected leave (with no catch-up upon return). Employers that would like to be more generous can establish leave policies to continue funding the HSA.

The one caveat is that these leave laws do require the employer to make HSA contributions to an employee on protected leave if the employer continues to make HSA contributions for employees on other forms of non-protected leave.

Summary

Even for employees protected leave, employers are not required to continue HSA contributions for the employee while on leave. If the employer chooses to continue to make HSA contributions to an employee on protected leave, it should do so on a consistent basis for all employees on protected leave (and only for those employees who maintain coverage under the employer-sponsored HDHP while on the leave).

For full details on the employer LOA health benefits considerations, see our Newfront Office Hours Webinar Health Benefits While On Leave: The Rules All Employers Need to Know.

Regulations

Newfront Office Hours - Health Benefits While on Leave

Health FSA Protected Leaves

DOL Field Assistance Bulletin 2004-01:

https://www.dol.gov/agencies/ebsa/employers-and-advisers/guidance/field-assistance-bulletins/2004-01

As noted above, HSAs are personal health care savings vehicles rather than a form of group health insurance.

…

Accordingly, we would not find that employer contributions to HSAs give rise to an ERISA-covered plan where the establishment of the HSAs is completely voluntary on the part of the employees and the employer does not: (i) limit the ability of eligible individuals to move their funds to another HSA beyond restrictions imposed by the Code; (ii) impose conditions on utilization of HSA funds beyond those permitted under the Code; (iii) make or influence the investment decisions with respect to funds contributed to an HSA; (iv) represent that the HSAs are an employee welfare benefit plan established or maintained by the employer; or (v) receive any payment or compensation in connection with an HSA.

The mere fact that an employer imposes terms and conditions on contributions that would be required to satisfy tax requirements under the Code or limits the forwarding of contributions through its payroll system to a single HSA provider (or permits only a limited number of HSA providers to advertise or market their HSA products in the workplace) would not affect the above conclusions regarding HSAs funded with employer or employee contributions, unless the employer or the HSA provider restricts the ability of the employee to move funds to another HSA beyond those restrictions imposed by the Code.

…

HSAs generally will not constitute “employee welfare benefit plans” for purposes of the provisions of Title I of ERISA.

FMLA

29 USC §2614(c)(1):

(c) Maintenance of health benefits.

_(1) _Coverage. Except as provided in paragraph (2), during any period that an eligible employee takes leave under section 102 (29 USC §2612), the employer shall maintain coverage under any “group health plan” (as defined in section 5000(b)(1) of the Internal Revenue Code of 1986) for the duration of such leave at the level and under the conditions coverage would have been provided if the employee had continued in employment continuously for the duration of such leave.

29 CFR §825.209(a):

**(a) **During any FMLA leave, an employer must maintain the employee’s coverage under any group health plan (as defined in the Internal Revenue Code of 1986 at 26 U.S.C. 5000(b)(1)) on the same conditions as coverage would have been provided if the employee had been continuously employed during the entire leave period. All employers covered by FMLA, including public agencies, are subject to the Act’s requirements to maintain health coverage. The definition of group health plan is set forth in §825.800.

29 CFR §825.209(h):

**(h) **An employee’s entitlement to benefits other than group health benefits during a period of FMLA leave (e.g., holiday pay) is to be determined by the employer’s established policy for providing such benefits when the employee is on other forms of leave (paid or unpaid, as appropriate).

29 CFR §825.210(a):

**(a) **Group health plan benefits must be maintained on the same basis as coverage would have been provided if the employee had been continuously employed during the FMLA leave period. Therefore, any share of group health plan premiums which had been paid by the employee prior to FMLA leave must continue to be paid by the employee during the FMLA leave period. If premiums are raised or lowered, the employee would be required to pay the new premium rates. Maintenance of health insurance policies which are not a part of the employer’s group health plan, as described in §825.209(a), are the sole responsibility of the employee. The employee and the insurer should make necessary arrangements for payment of premiums during periods of unpaid FMLA leave.

PDL

Cal Gov Code § 12945(a)(2)(A):

(a) In addition to the provisions that govern pregnancy, childbirth, or a related medical condition in Sections 12926 and 12940, each of the following shall be an unlawful employment practice, unless based upon a bona fide occupational qualification:

…

**(2)**undefined

** **

CFRA

2 CCR § 11092(c):

(c) Provision of Health Benefits.

If the employer provides health benefits under any group health plan, the employer has an obligation to continue providing such benefits during an employee’s CFRA leave, FMLA leave, or both. The following rules apply:

(1) The employer shall maintain and pay for an employee’s health coverage at the same level and under the same conditions as coverage would have been provided if the employee had not taken CFRA leave.

(2) The employer’s obligation commences on the date leave first begins under CFRA for the duration of the leave, up to a maximum of 12 workweeks in a 12-month period. As section 11044(c) of the Council’s pregnancy disability leave regulations state, “The time that an employer maintains and pays for group health coverage during pregnancy disability leave shall not be used to meet an employer’s obligation to pay for 12 weeks of group health coverage during leave taken under CFRA. This shall be true even where an employer designates pregnancy disability leave as family and medical leave under FMLA. The entitlements to employer-paid group health coverage during pregnancy disability leave and during CFRA are two separate and distinct entitlements.”

(3) A “group health plan” is as defined in section 5000(b)(1) of the Internal Revenue Code of 1986. If the employer’s group health plan includes dental care, eye care, mental health counseling, or other types of coverage, or if it includes coverage for an employee’s dependents as well as for the employee, the employer shall also continue this coverage.

(4) Although the employer’s obligation to continue group health benefits under either FMLA or CFRA, or both, does not exceed 12 workweeks in a 12-month period, nothing shall preclude the employer from maintaining and paying for health care coverage for longer than 12 workweeks.

(5) An employer may recover the premium that the employer paid for maintaining group health care coverage during any unpaid part of the CFRA leave if both of the following conditions occur:undefinedundefined

(6) Group health plan coverage must be maintained for an employee on CFRA leave until:undefinedundefined

(C) The employee provides unequivocal notice of intent not to return to work

Brian Gilmore

Lead Benefits Counsel, VP, Newfront

Brian Gilmore is the Lead Benefits Counsel at Newfront. He assists clients on a wide variety of employee benefits compliance issues. The primary areas of his practice include ERISA, ACA, COBRA, HIPAA, Section 125 Cafeteria Plans, and 401(k) plans. Brian also presents regularly at trade events and in webinars on current hot topics in employee benefits law.

Connect on LinkedIn