ACA Employer Mandate and Outside Staffing Firms

By Brian Gilmore | Published June 7, 2019

Question: How does the ACA employer mandate apply to workers hired through an outside staffing firm?

Compliance Team Response:

ACA Employer Mandate: Applies to Common-Law Employees

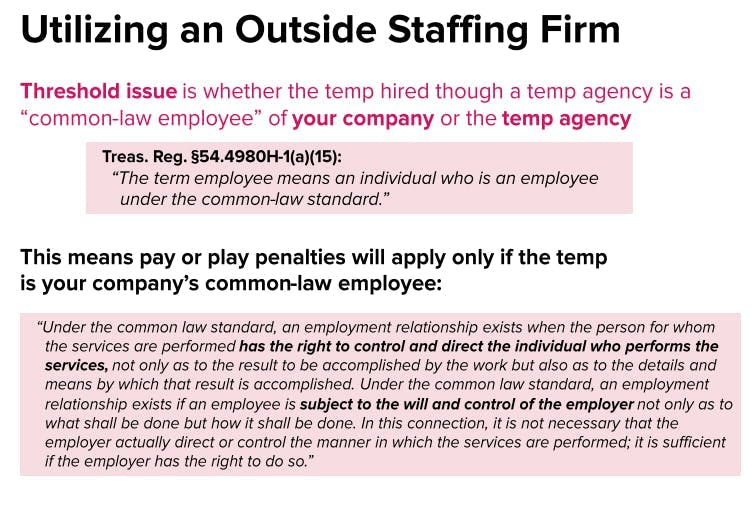

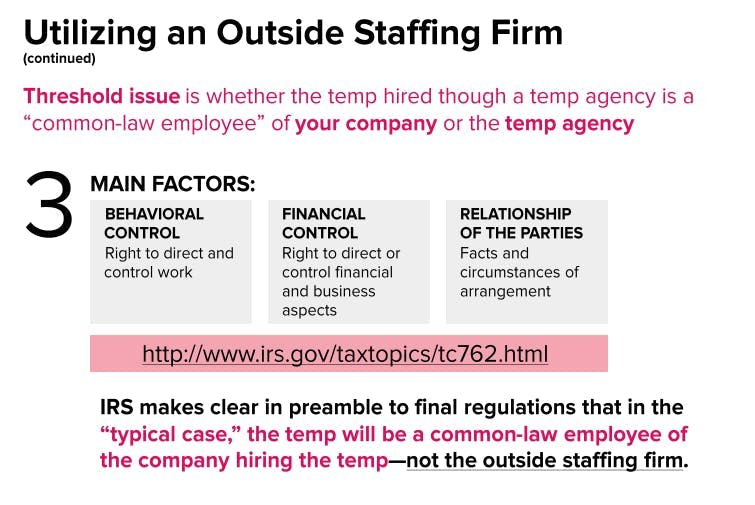

The ACA employer mandate rules apply only to an employer’s common-law employees.

ACA Employer Mandate: Workers Payrolled Through an Outside Staffing Firm

Full-time workers hired through an outside staffing firm are in almost all cases still common-law employees of the worksite employer. For ACA purposes, this means that the employer’s obligation to offer health coverage to avoid potential penalties still applies to any form of contingent worker hired through an outside staffing firm.

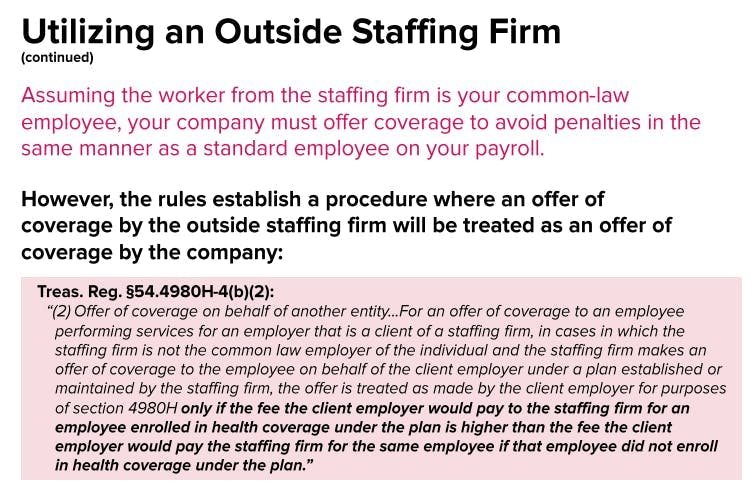

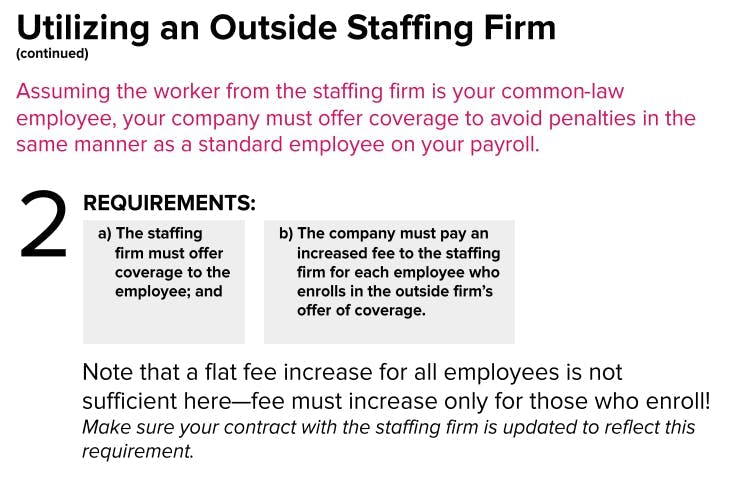

Fortunately, the ACA rules permit the employer to delegate the offer of coverage requirement to the outside staffing firm. In other words, just as the employer will delegate many administrative and recordkeeping duties to the outside staffing firm for other purposes (e.g., payroll, Forms W-2), the employer can also assign the offer of coverage responsibility to the outside staffing firm.

The employer mandate regulations set forth two requirements for employers to avoid potential penalties for outside staffing firm workers without offering coverage under the employer’s group health plan:

The outside staffing firm offers coverage meeting ACA standards to full-time workers, and

The outside staffing firm charges the employer an additional fee for those workers who elect to enroll in the outside staffing firm’s offer of coverage.

This will result in the employer being treated as having offered coverage to the outside staffing firm workers, even though the employer isn’t offering coverage under its group health plan. It’s essentially an imputed offer of coverage through the outside staffing firm where the employer’s arrangement satisfies the two requirements above.

The actual amount of the additional fee charged for those who enroll in the outside staffing firm’s offer of coverage is not specified in the rules and is subject to negotiation between the employer and outside staffing firm. While the amount of this additional fee does not necessarily need to track the actual cost to the outside staffing firm of enrolling the worker in coverage, employers should be cautious to ensure that the amount is not so low as to be perceived as nominal.

Can the Employer Provide for Eligibility Under Its Group Health Plan to Outside Staffing Firm Workers?

In theory, this is an option because the workers are typically common-law employees of the employer.

However, the only way that these employees could pay for the employer’s coverage on a pre-tax basis would be if the outside staffing firm permitted the salary reduction contributions through its Section 125 cafeteria plan. The outside staffing firm generally will not permit that approach because the contribution would not be for the outside staffing firm’s plan.

Assuming pre-tax payment through the outside staffing firm’s cafeteria plan is not an option, the only way to make this work is by having the employee pay the employee-share of the premium on an after-tax basis outside of payroll in a manner similar to COBRA premium payments. The employer could choose to gross-up the employees payrolled through the outside staffing firm for the taxes on their premium contributions (assuming this is permitted by the outside staffing firm).

In general, it is administratively easier to have the outside staffing firm employees instead participate in the outside staffing firm’s benefits. This is by far the most common approach.

What About (Properly Classified) Independent Contractors?

The ACA employer mandate does not apply to properly classified independent contractors. In fact, it generally is not an option to offer coverage to independent contractors regardless.

Keep in mind that the ACA employer mandate is just one of many reasons why it is extremely important to properly classify workers as independent contractors or common-law employees.

For more details:

Newfront ACA Employer Mandate Pay or Play and ACA Reporting Guide

Utilizing an Outside Staffing Firm

Utilizing an Outside Staffing Firm Main Factors

Utilizing an Outside Staffing Firm Rules

Utillizing an Outside Staffing Firm Requirements

Regulations

Treas. Reg. §54.4980H-1(a)(15):

(15) Employee. The term employee means an individual who is an employee under the common-law standard. See §31.3401(c)-1(b). For purposes of this paragraph (a)(15), a leased employee (as defined in section 414(n)(2)), a sole proprietor, a partner in a partnership, a 2-percent S corporation shareholder, or a worker described in section 3508 is not an employee.

Treas. Reg. §54.4980H-4(b)(2):

(2) Offer of coverage on behalf of another entity. For purposes of section 4980H, an offer of coverage by one applicable large employer member to an employee for a calendar month is treated as an offer of coverage by all applicable large employer members for that calendar month. In addition, an offer of coverage made to an employee on behalf of a contributing employer under a multiemployer or single employer Taft-Hartley plan or multiple employer welfare arrangement (MEWA) is treated as made by the employer. For an offer of coverage to an employee performing services for an employer that is a client of a staffing firm, in cases in which the staffing firm is not the common law employer of the individual and the staffing firm makes an offer of coverage to the employee on behalf of the client employer under a plan established or maintained by the staffing firm, the offer is treated as made by the client employer for purposes of section 4980H only if the fee the client employer would pay to the staffing firm for an employee enrolled in health coverage under the plan is higher than the fee the client employer would pay the staffing firm for the same employee if that employee did not enroll in health coverage under the plan.

79 Fed. Reg. 8543, 8566 (Feb. 12, 2014):

https://www.govinfo.gov/content/pkg/FR-2014-02-12/pdf/2014-03082.pdf

Under this same reasoning, if certain conditions are met, an offer of coverage to an employee performing services for an employer that is a client of a professional employer organization or other staffing firm (in the typical case in which the professional employer organization or staffing firm is not the common law employer of the individual) (referred to in this section IX.B of the preamble as a “staffing firm”) made by the staffing firm on behalf of the client employer under a plan established or maintained by the staffing firm, is treated as an offer of coverage made by the client employer for purposes of section 4980H. For this purpose, an offer of coverage is treated as made on behalf of a client employer only if the fee the client employer would pay to the staffing firm for an employee enrolled in health coverage under the plan is higher than the fee the client employer would pay to the staffing firm for the same employee if the employee did not enroll in health coverage under the plan.

Newfront Model Outside Staffing Firm Agreement Provision:

Staffing Firm will offer all Staffing Firm Workers who work at the Company on a full-time basis, as defined pursuant to the ACA and Treas. Reg. §54.4980H-3, the opportunity to enroll in health coverage for themselves and their dependents (including at least the ACA requirement of natural children, adopted children, and children lawfully placed for legal adoption to age 26). Such health coverage shall, within the meaning of the ACA and Treas. Reg. §54.4980H-1 et seq., be “minimum essential coverage” that is “affordable” and provide “minimum value” to the Staffing Firm Workers. Staffing Firm will offer such health coverage to applicable full-time Staffing Firm Workers with an effective date that is no later than the first day of the fourth full calendar month in which such Staffing Firm Workers work at the Company. For each Staffing Firm Worker who elects to enroll in such offer of health coverage, Staffing Firm shall charge the Company an additional fee that is mutually agreed upon in writing between Staffing Firm and the Company. Staffing Firm shall be responsible for all ACA health information reporting under IRC §6055 and IRC §6056, as reported via IRS Forms 1094-C and 1095-C, related to such Staffing Firm Workers. In addition to any other indemnification provisions set forth in this Agreement, Staffing Firm shall indemnify the Company for any and all penalties (including, but not limited to, assessable payments under IRC §4980H, §6055, and §6056) that are assessed to the Company on account of the Staffing Firm’s failure to offer such health coverage to or complete such health information reporting related to any Staffing Firm Workers who work at the Company.

Brian Gilmore

Lead Benefits Counsel, VP, Newfront

Brian Gilmore is the Lead Benefits Counsel at Newfront. He assists clients on a wide variety of employee benefits compliance issues. The primary areas of his practice include ERISA, ACA, COBRA, HIPAA, Section 125 Cafeteria Plans, and 401(k) plans. Brian also presents regularly at trade events and in webinars on current hot topics in employee benefits law.

Connect on LinkedIn