HSA Limit for Partial-Year Family Coverage

By Brian Gilmore | Published June 15, 2018

Question: An employee who began the year in employee-only HDHP coverage was recently married and enrolled her new spouse mid-year. What is the HSA contribution limit for HSA-eligible individuals enrolled part of the year in employee-only HDHP coverage, and part of the year in family HDHP coverage?

Compliance Team Response:

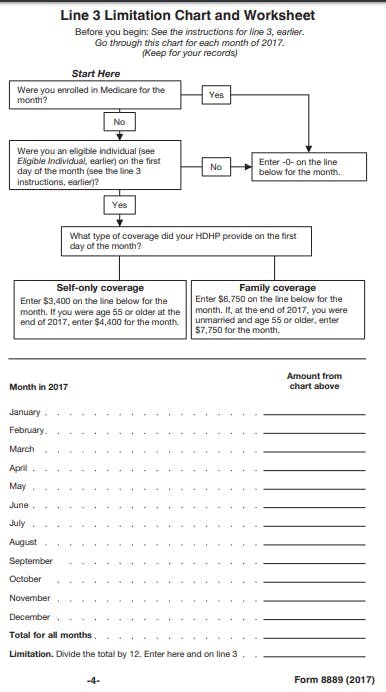

The HSA contribution limits are calculated on a monthly basis. This means the employee is able to contribute 1/12 of the employee-only limit for the months of the year in employee-only HDHP coverage, and 1/12 of the family limit for the months of the year in family HDHP coverage.

The employee’s overall annual contribution limit is the sum of those two prorated employee-only and family contribution numbers.

You look to the coverage in effect as of the first day of each calendar month to determine whether the employee has employee-only or family HDHP coverage for that month

The IRS has a chart to handle this calculation on page four of the Form 8889 Instructions. You just need to adjust the numbers for the current-year contribution limits.

For more details on how the HSA contribution limit applies in other situations, see slides 11-18 of our Newfront Office Hours webinar Go All the Way With HSA: Everything HDHP/HSA You Need to Know.

Regulations:

IRS Form 8889 Instructions:

https://www.irs.gov/pub/irs-pdf/i8889.pdf

** **

IRC §223(b)(2):

(2) Monthly limitation.

The monthly limitation for any month is 1/12 of—

(A) in the case of an eligible individual who has self-only coverage under a high deductible health plan as of the first day of such month, $2,250.

(B) in the case of an eligible individual who has family coverage under a high deductible health plan as of the first day of such month, $4,500.

Brian Gilmore

Lead Benefits Counsel, VP, Newfront

Brian Gilmore is the Lead Benefits Counsel at Newfront. He assists clients on a wide variety of employee benefits compliance issues. The primary areas of his practice include ERISA, ACA, COBRA, HIPAA, Section 125 Cafeteria Plans, and 401(k) plans. Brian also presents regularly at trade events and in webinars on current hot topics in employee benefits law.

Connect on LinkedIn